The Unified Payments Interface (UPI) completely revolutionized urban transactions over the last decade, turning India into a global leader in real-time digital payments. However, the true frontier of financial inclusion is unfolding in rural landscapes. With the introduction of UPI 2.0 and specialized frameworks like UPI 123Pay (for feature phones) and UPI Lite (for low-value offline transactions), the digital payment ecosystem has penetrated tier-3 cities, villages, and remote micro-economies.

This comprehensive guide breaks down the underlying technical architecture of UPI’s rural expansion, evaluates how offline digital payment frameworks overcome infrastructure gaps, and analyzes the profound socioeconomic impact on rural merchants.

1. Architectural Upgrades: What Makes UPI 2.0 Rural-Ready?

The initial launch of UPI relied heavily on seamless smartphone access, stable 4G/5G mobile data, and active bank account linking. In rural areas, this created immediate friction due to intermittent network connectivity and lower smartphone penetration. UPI 2.0 and its subsequent expansions introduced core architectural changes to bypass these limitations:

- Delegated Payments: This protocol allows a primary account holder (e.g., a family member with a smartphone) to authorize a secondary user (e.g., a relative with a feature phone) to initiate transactions up to a certain limit from the main account.

- Single-Block, Multiple-Debit: Rural consumers can block a specific amount in their bank account for a milestone-based service—such as purchasing agricultural seeds or fertilizers—and have the funds debited gradually as deliveries are made, fostering immense trust.

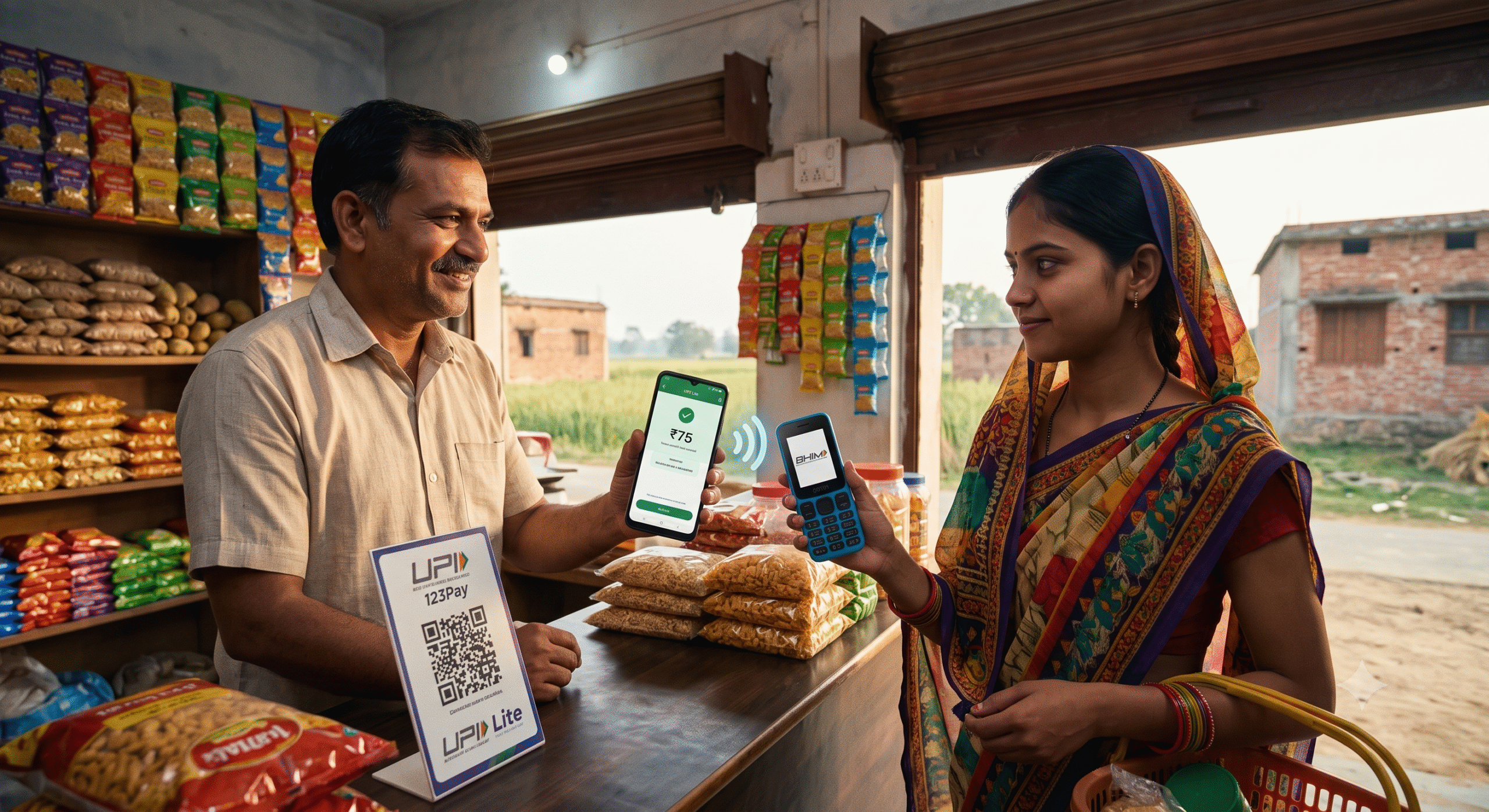

- The UPI Lite On-Device Wallet: By shifting small-value transactions (under ₹500) from the core banking system to an isolated local wallet directly on the device, UPI drastically reduced the load on bank servers.

Technical Note: UPI Lite transactions succeed even during peak hours or near-total bank server downtime because they execute locally on the device using a pre-funded balance, syncing with the main ledger asynchronously.

2. Overcoming the Connectivity Barrier: Offline Digital Frameworks

The core challenge of rural fintech is operating in dark zones—areas completely devoid of internet connectivity. To solve this, the National Payments Corporation of India (NPCI) deployed alternative communication channels that don’t require an internet connection:

| Framework | Core Communication Technology | User Experience / Interface | Target Audience |

| UPI 123Pay (IVR) | Standard Voice Calls via Interactive Voice Response | Automated telephonic prompts requiring DTMF (dual-tone multi-frequency) keypad inputs. | Feature phone users in low-connectivity areas. |

| UPI 123Pay (Missed Call) | Dual-Stage Missed Call Protocol | Giving a missed call to a merchant-specific number triggers a secure, automated callback to authorize payments via UPI PIN. | Small roadside vendors and daily wage earners. |

| UPI 123Pay (Proximity Sound) | Contactless Sound Wave Technology | Devices emit a localized ultrasonic sound wave containing encrypted transaction data between buyer and seller devices. | Rural merchants operating crowded, off-grid weekly markets. |

3. Socioeconomic Impact: Transforming the Rural Merchant Ecosystem

By removing the reliance on physical cash, these technical frameworks have fundamentally shifted the economic reality of rural businesses:

A. Formal Credit Creation

Historically, small rural merchants operated entirely in cash, leaving no verifiable paper trail. Because banks could not assess their creditworthiness, these business owners were forced to rely on predatory local moneylenders for working capital. Today, every micro-transaction passing through a UPI QR code builds a structured, immutable financial history. Digital ledger trails allow formal financial institutions to offer instant, low-interest merchant loans based on predictable daily cashflows.

B. Velocity of Capital

In a cash-based rural economy, a merchant must physically travel to a wholesale market in a neighboring town to restock goods, wasting valuable business hours and risking theft. Automated UPI transfers allow rural shopkeepers to pay suppliers instantly from their doorstep, ensuring that inventory moves faster and capital is recycled into the business immediately.

C. Frictionless Agriculture Supply Chains

Agriculture is the backbone of the rural economy. When farmers sell their yields to local procurement centers, cash distribution can take days or weeks. With integrated UPI payment gateways built directly into agricultural management platforms, farmers receive direct, instantaneous bank transfers the moment their crop weight is logged into the system.

4. Remaining Challenges: Navigating Security and the Digital Divide

Despite massive strides, deep integration faces structural roadblocks that tech developers and financial institutions are actively trying to solve:

- Digital Literacy & Social Engineering: The primary bottleneck is no longer software uptime, but user vulnerability. Rural users are frequently targeted by voice-phishing (vishing) scams where fraudsters trick individuals into entering their UPI PIN under the guise of “receiving a lottery payout.”

- Localized Language Support: While systems like IVR support multiple regional languages, complex error messages or dispute resolution interfaces can still alienate users who are non-literate or speak localized dialects.

- The Smart vs. Feature Phone Divide: While UPI 123Pay has bridged the hardware gap, the feature-rich merchant tools (inventory tracking, dynamic QR codes, analytics) are still heavily skewed toward smartphone users, leaving basic feature phone users with simple transaction capabilities.

5. The Path Ahead: The Future of Deep-Rural Fintech

The next phase of India’s rural digital transformation will rely heavily on localized edge computing and advanced artificial intelligence. We are moving toward an era of Voice-Activated Conversational Banking, where a user can simply speak into a basic phone in their native dialect—“Transfer three hundred rupees to the grocery store”—and an localized AI voice bot will securely handle the parsing, translation, and execution of the UPI transaction protocol.

By turning the mobile phone into a self-contained digital bank, UPI 2.0 is doing far more than replacing paper currency; it is democratizing access to wealth, dismantling geographic barriers, and ensuring that the financial heartbeat of rural India beats in perfect synchronization with the rest of the world.

Reference Links

- Reserve Bank of India (RBI) Notifications: https://www.rbi.org.in/

- Ministry of Electronics and Information Technology (MeitY): https://www.meity.gov.in/

+ There are no comments

Add yours