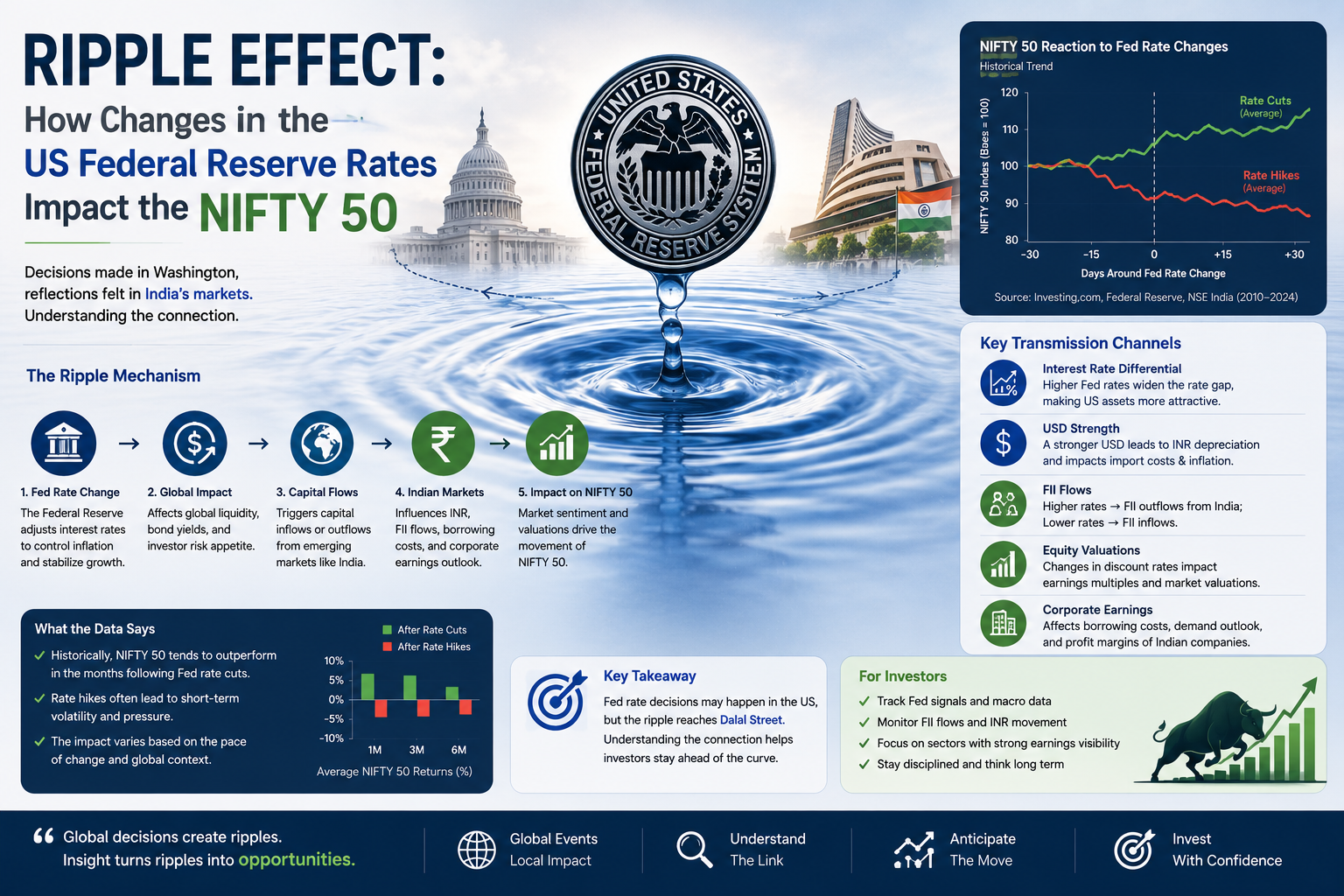

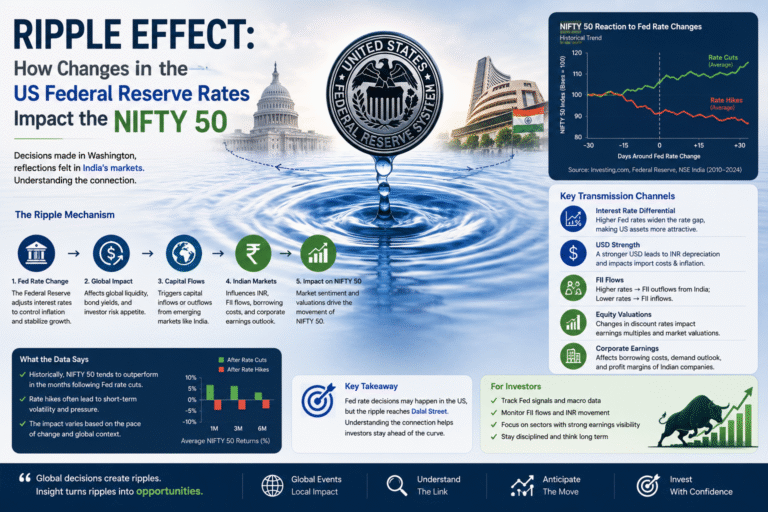

In an interconnected global financial system, no capital market operates in isolation. For domestic investors tracking India’s benchmark NIFTY 50 index, some of the most critical market triggers originate thousands of miles away inside the boardroom of the US Federal Reserve.

When the Fed adjusts its target federal funds rate—or signals a shift in its monetary stance—it triggers an immediate reallocation of global capital. With the Fed keeping its policy rate steady in the 3.50%–3.75% range to combat inflation, understanding the precise transmission channels between Washington’s monetary policies and Mumbai’s trading floors is vital.

This analytical guide breaks down the core mechanics of how US interest rate cycles drive foreign fund flows, influence the Indian Rupee, and impact specific sectors within the NIFTY 50.

1. The FII Transmission Channel: The Quest for Yield

The most direct link between US interest rates and the Indian stock market is the movement of Foreign Institutional Investors (FIIs), often referred to as Hot Capital.

[US Federal Reserve Hikes Rates] ──► US Treasury Yields Rise ──► Capital Retreats from Emerging Markets

│

▼

[NIFTY 50 Appreciates / Capital Inflow] ◄── FIIs Seek High-Growth Alternatives ◄── [Fed Lowers Rates]

- The Rate Hike/High-Yield Phase: When US interest rates are elevated or rising, the yields on risk-free US Treasury bonds climb. Global institutional investors naturally de-risk their portfolios by pulling capital out of emerging markets like India and redirecting it back to the US. This sudden exit of foreign capital can create immediate selling pressure on index-heavy NIFTY components.

- The Rate Cut/Dovish Phase: Conversely, when the Fed cuts rates or adopts a dovish tone, the yield on US bonds drops. Seeking higher returns, global funds look toward structurally strong, high-growth alternatives. India’s diversified, consumption-driven economy stands out as a prime destination, driving robust FII inflows that fuel sustained domestic market rallies.

2. The Currency Vector: Imported Inflation and Corporate Margins

Federal Reserve policies exert massive influence over the US Dollar Index (DXY), which shares an inverse relationship with the Indian Rupee (INR).

- The Strong Dollar Trap: Higher US interest rates strengthen the greenback. A depreciating rupee increases the landed cost of India’s dollar-denominated imports—most notably crude oil. For NIFTY companies reliant on imported raw materials, this “imported inflation” squeezes gross corporate margins, dragging down broader market earnings.

- The Valuation Re-rating: Persistent domestic currency depreciation forces the Reserve Bank of India (RBI) to maintain elevated domestic repository rates to protect the currency, even if local growth conditions warrant a cut. This limits credit expansion and can damp corporate valuations across capital-intensive sectors.

3. Asymmetric Sectoral Impact within the NIFTY 50

A shift in Fed policy does not impact all NIFTY 50 companies equally. The index experiences sharp shifts between export-driven defensives and domestic cyclical sectors:

A. Export-Oriented Defensives (IT and Pharmaceuticals)

India’s frontline Information Technology (IT) and pharmaceutical firms generate a vast majority of their revenue in US Dollars.

- The Impact: When interest rates remain high and the dollar strengthens, these sectors technically enjoy a short-term boost in rupee-denominated earnings upon repatriation.

- The Stretched Valuation Risk: However, if high US rates trigger a broader cooling of corporate tech spending in western markets, the long-term order pipeline dries up. Stretched IT valuations face rapid corrections as global capital reallocates away from tech frenzy to safe-haven alternatives.

B. Rate-Sensitive Cyclicals (Banking, Auto, and Realty)

Domestic cyclicals are highly dependent on domestic credit availability and consumer borrowing costs.

- The Impact: When global macroeconomic pressures recede and capital flows turn positive, these sectors do the heavy lifting for the NIFTY 50. Leading private and public banks benefit from robust corporate credit demand, while stable currency dynamics boost consumer durables, real estate, and automotive sales.

4. NIFTY 50 Historical Resilience: Evaluating the Drawdowns

While a sudden hawkish shift by the Fed can spark short-term panic, historical market data suggests that corrections driven by external global shocks are typically temporary.

| Market Metric | Average Historical Observation | Investor Implication |

| Average Annual Drawdown | $\approx 18\%$ Volatility Margin | Normal market cycle behavior; external shocks rarely break structural growth trends permanently. |

| Typical Recovery Window | $12\text{ to }14\text{ Months}$ Post-Fall | Markets historically claw back losses driven by FII exits once domestic earnings recover. |

| Post-Correction Return | $\approx 32\%$ Alpha Growth in Year 2 | Staggered accumulation during global market stress offers superior long-term entry points. |

5. Strategy for Navigating Global Monetary Cycles

For long-term participants in the Indian equity markets, trying to time entry points based on every Federal Reserve press conference is a losing battle. The most effective defense against global macro volatility is a staggered investment approach focused heavily on businesses with visible earnings growth, robust domestic moats, and structural capital expenditure support.

When global macro anxieties cloud near-term sentiment, it creates a valuation gap where fundamentally sound companies trade well below their long-term fair value—offering disciplined investors an ideal opportunity to accumulate quality assets ahead of the next structural market rebound.

Reference Links

- U.S. Federal Reserve Monetary Policy Releases: https://www.federalreserve.gov/

- National Stock Exchange of India (NSE): https://www.nseindia.com/

- FRED Economic Data (St. Louis Fed): https://fred.stlouisfed.org/

+ There are no comments

Add yours