Key Highlights

- ₹3.48 lakh crore cumulative savings achieved between 2013-2024 by eliminating ghost beneficiaries and reducing leakages through Aadhaar-based authentication

- Welfare Efficiency Index surge from 0.32 in 2014 to 0.91 in 2023, demonstrating dramatic improvement in targeted delivery and fiscal optimization

- 176 crore beneficiaries coverage achieved by 2024, representing 16-fold growth from 11 crore in 2013 without proportional spending increase

- JAM Trinity success with 53.13 crore Jan Dhan accounts opened, enabling seamless integration of banking, identity, and mobile connectivity

- COVID-19 resilience demonstrated through ₹27,442 crore transferred to 11.42 crore beneficiaries during lockdown, ensuring critical welfare continuity

Transforming Welfare Delivery Through Technology

Direct Bank Transfer (DBT) represents one of India’s most ambitious governance reforms, fundamentally transforming how government subsidies, benefits, and entitlements reach beneficiaries. Launched on January 1, 2013, this electronic transfer system aims to eliminate intermediaries, reduce corruption, and ensure transparent delivery of welfare benefits directly into beneficiaries’ bank accounts.

The DBT system addresses critical challenges that plagued traditional welfare delivery: leakages, pilferage, corruption, and delays that prevented intended recipients from receiving their rightful benefits. By leveraging technology, particularly the JAM (Jan Dhan-Aadhaar-Mobile) trinity, DBT has created a robust framework for efficient, transparent, and inclusive welfare distribution.

As Finance Minister Nirmala Sitharaman emphasized, “DBT has revolutionized welfare delivery in India, by plugging leakages and ensuring transparency. Over 1,200 government schemes now leverage DBT, enabling direct transfer of ₹44 lakh crore to beneficiaries’ bank accounts”. This transformation represents not just technological advancement but a fundamental shift toward accountable governance and dignified service delivery.

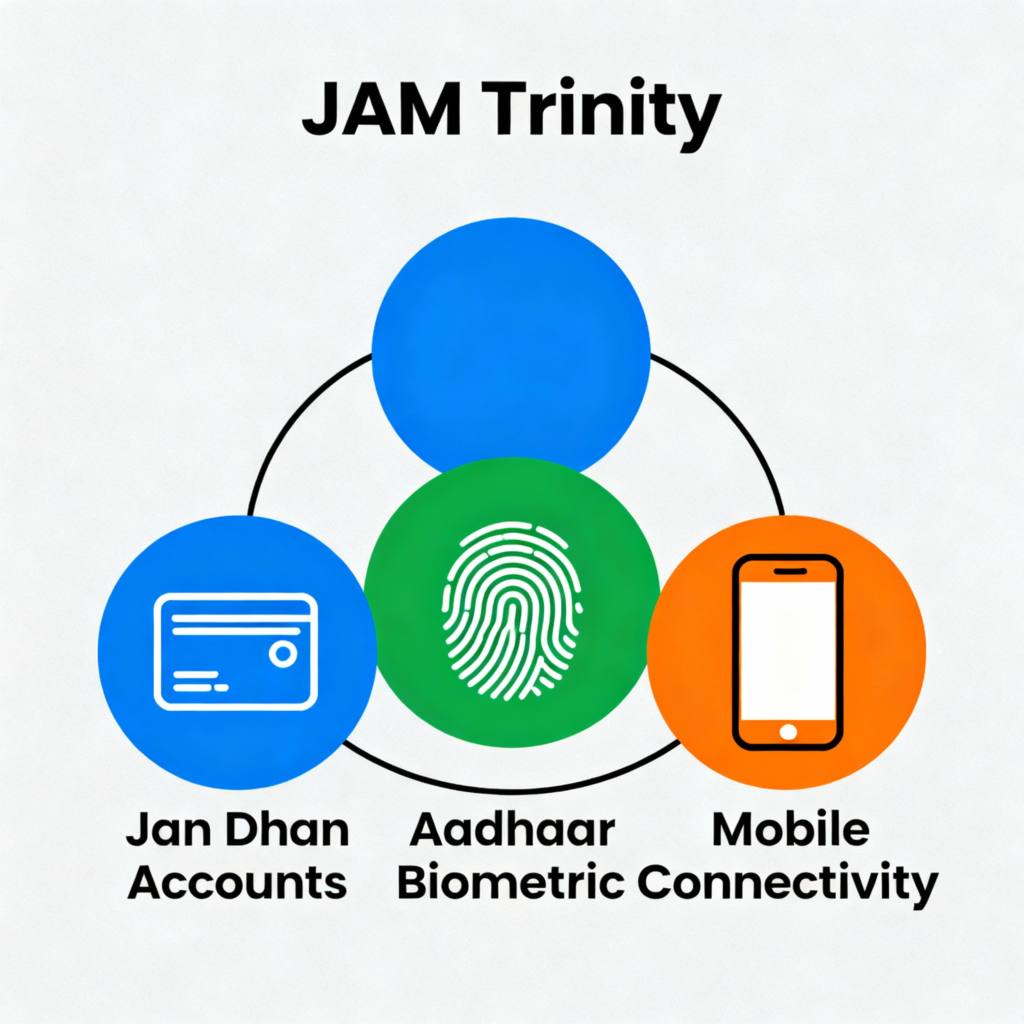

The JAM Trinity: Foundation of Digital Transformation

Jan Dhan Yojana: Universal Banking Access

The Pradhan Mantri Jan Dhan Yojana (PMJDY), launched in August 2014, forms the cornerstone of financial inclusion enabling DBT’s success. This world’s largest financial inclusion program has opened 55.44 crore accounts by 2025, with 67% in rural and semi-urban areas and 56% owned by women. pib.gov

PMJDY Achievements:

- Zero-balance accounts with overdraft facility up to ₹10,000

- RuPay debit cards providing accident insurance coverage of ₹2 lakh

- Direct access to banking services for previously unbanked populations

- Gender empowerment through women-centric account ownership

Aadhaar: Unique Identity Framework

Aadhaar, the world’s largest biometric identification system, provides the authentication backbone for DBT operations. By 2023, over 1.3 billion Aadhaar numbers have been issued, with over 80% of PMJDY accounts linked to Aadhaar for seamless benefit delivery. pib.gov

The Aadhaar-based authentication system eliminates duplicate and ghost beneficiaries, ensuring only genuine recipients receive benefits. This digital identity framework has been instrumental in achieving the ₹3.48 lakh crore savings by preventing fraudulent claims and ensuring accurate targeting.

Mobile Connectivity: Digital Bridge

Mobile connectivity serves as the vital communication link, enabling real-time notifications, banking access, and service delivery even in remote areas. The widespread mobile penetration has facilitated SMS confirmations, mobile banking, and digital literacy development among beneficiaries.

Major DBT Schemes: Transformative Impact Across Sectors

MGNREGA: Employment Guarantee Revolution

The Mahatma Gandhi National Rural Employment Guarantee Scheme demonstrates DBT’s transformative impact on employment programs. 98% of wages are now transferred timely, saving ₹42,534 crore through DBT-driven accountability. This direct transfer mechanism has eliminated payment delays and corruption by transferring wages directly to workers’ accounts.

MGNREGA DBT Benefits:

- Elimination of middlemen and local-level corruption

- Improved timeliness with 98% on-time payments

- Enhanced transparency through digital audit trails

- Boosted worker confidence leading to increased participation

PM-KISAN: Direct Income Support

Launched in 2019, PM-KISAN provides ₹6,000 annual income support to small and marginal farmers through direct bank transfers. The scheme has saved ₹22,106 crore by deleting 2.1 crore ineligible beneficiaries, demonstrating effective targeting through Aadhaar authentication.

PM-KISAN Impact:

- ₹3 lakh crore disbursed to nearly 11 crore farmers as of March 2025

- Three equal installments ensuring regular income support

- Digital record tracking of landholding patterns and eligibility

- Enhanced formal banking engagement among rural farmers

PAHAL: LPG Subsidy Transformation

The Pratyaksh Hanstantrit Labh (PAHAL) scheme became one of the world’s largest cash transfer programs by transferring LPG subsidies directly to consumers. By linking Aadhaar with consumer numbers and bank accounts, PAHAL successfully curbed duplicate and fake connections while ensuring transparent subsidy delivery.

PAHAL Achievements:

- World’s largest cash transfer program status

- Elimination of duplicate connections through Aadhaar linking

- Transparent subsidy delivery directly to bank accounts

- Reduced administrative costs and improved efficiency

Quantified Impact: Welfare Efficiency Revolution

Financial Savings and Fiscal Optimization

DBT has delivered remarkable fiscal consolidation without compromising welfare commitments. Subsidy allocations have halved from 16% to 9% of total government expenditure since DBT implementation, while beneficiary coverage expanded dramatically.

Sectoral Savings Breakdown:

- Food subsidies: ₹1.85 lakh crore (53% of total savings)

- MGNREGA: ₹42,534 crore through accountability improvements

- PM-KISAN: ₹22,106 crore by eliminating ineligible beneficiaries

- Overall leakage reduction: Over 90 million fake beneficiaries eliminated

Welfare Efficiency Index: Measuring Success

The Welfare Efficiency Index (WEI), a composite metric combining fiscal outcomes with social indicators, demonstrates DBT’s comprehensive impact. The WEI rose from 0.32 in 2014 to 0.91 in 2023, reflecting threefold improvement in both effectiveness and inclusion.

WEI Components:

- Fiscal savings and reduced administrative costs

- Beneficiary coverage expansion and targeting accuracy

- Social outcomes including women empowerment and rural development

- Transparency improvements and accountability mechanisms

Technological Innovations

e-RUPI: Purpose-Specific Digital Vouchers

Launched on August 2, 2021, e-RUPI represents the next evolution in DBT effectiveness. This cashless and contactless digital payment mechanism delivers vouchers to beneficiaries’ mobile phones as QR codes or SMS strings for specific purposes.

e-RUPI Advantages:

- Purpose-specific payments ensuring funds used for intended purposes

- No card, app, or internet banking requirement for redemption

- Enhanced targeting and leakage prevention

- End-to-end transparency in benefit delivery

e-RUPI Applications:

- Healthcare services under Ayushman Bharat and PM-JAY

- Mother and child welfare program deliveries

- TB eradication and nutrition support programs

- Educational scholarships and skill development vouchers

Digital Payment Integration

DBT’s integration with UPI and digital payment systems has facilitated seamless transactions while promoting digital literacy and financial inclusion. However, rural digital adoption remains challenging due to infrastructure limitations, digital literacy gaps, and trust issues.

Challenges and Implementation Barriers

Banking Infrastructure Deficits

Despite significant progress, banking infrastructure gaps in remote and rural areas continue posing challenges. Limited access to bank branches and cash-out points (COPs) makes fund withdrawal difficult for beneficiaries in remote regions

Infrastructure Challenges:

- 40% of households faced cash withdrawal issues during COVID-19 pandemic

- Limited availability of COPs in remote areas

- Technical failures in network and biometric authentication

- Instances of fraud and misconduct by banking agents

Digital Literacy and Exclusion Errors

Digital literacy gaps particularly affect rural populations, preventing effective utilization of DBT services. Nearly 27% of rural adults remain financially illiterate according to NABARD, limiting their ability to access digital banking platforms.

Exclusion Challenges:

- Aadhaar-related mismatches causing benefit delays

- Biometric authentication failures for elderly and disabled

- Limited smartphone access and internet connectivity

- Language barriers in digital interfaces

Vulnerable Group Access

Women, elderly citizens, tribal populations, and persons with disabilities face specific challenges in accessing DBT benefits. Only 30% of rural women have access to formal financial services, limiting DBT’s reach among female beneficiaries.

COVID-19: DBT’s Crisis Response Excellence

The COVID-19 pandemic provided the ultimate test of DBT’s resilience and effectiveness. Between March and April 2020, the system transferred ₹27,442 crore to 11.42 crore beneficiaries under various relief schemes, demonstrating its capacity for rapid emergency response.

Pandemic Response Statistics:

- Central schemes: ₹27,442 crore to 11.42 crore beneficiaries

- State schemes: ₹9,217 crore to 4.59 crore beneficiaries through 180 programs

- Total FY 2020-21: ₹1,41,714 crore to 47 crore beneficiaries by October 2020

This crisis response highlighted DBT’s role as India’s social safety net backbone, providing immediate relief to vulnerable populations during unprecedented challenges.

Policy Recommendations and Way Forward

Infrastructure Development Priorities

Last-Mile Connectivity:

- Expand banking correspondent networks in remote areas

- Strengthen digital infrastructure with reliable internet connectivity

- Establish more cash-out points and banking service centers

- Implement mobile banking vans for periodic service delivery

Digital Literacy and Capacity Building

Comprehensive Training Programs:

- Community-based digital literacy initiatives

- Local language interfaces for banking and government applications

- Women-focused training programs addressing gender disparities

- Elder-friendly service designs accommodating physical limitations

Technology Enhancement

System Improvements:

- Robust cybersecurity frameworks protecting beneficiary data

- AI-powered fraud detection systems

- Blockchain integration for enhanced transparency

- Real-time grievance redressal mechanisms

Policy Framework Strengthening

Regulatory Reforms:

- Data protection legislation ensuring privacy rights

- Standardized KYC procedures reducing documentation barriers

- Interoperability standards across payment systems

- Regular impact assessments and scheme optimization

Global Recognition and Future Prospects

International Acclaim

DBT has garnered significant international recognition for its scale and impact. The IMF has hailed DBT as “a logistical marvel” reaching hundreds of millions at low-income levels, while the World Bank has praised its ability to provide support to 85% of rural households and 69% of urban households.

Future Expansion Plans

Emerging Applications:

- Healthcare service delivery through digital health vouchers

- Educational scholarships with purpose-specific targeting

- Disaster relief mechanisms for rapid emergency response

- Agricultural input subsidies with real-time tracking

Technology Integration:

- Artificial Intelligence for predictive analytics and targeting

- Internet of Things for real-time monitoring

- Blockchain technology for immutable transaction records

- Machine Learning for fraud detection and prevention

Conclusion: DBT as Governance Game-Changer

Direct Benefit Transfer has emerged as a transformative force in India’s social sector governance, delivering unprecedented efficiency, transparency, and inclusion in welfare delivery. The ₹3.48 lakh crore savings and 16-fold beneficiary expansion demonstrate DBT’s capacity to optimize fiscal resources while expanding social protection.

The JAM Trinity’s success in creating universal banking access, unique identity verification, and mobile connectivity has laid the foundation for Digital India’s inclusive growth. From MGNREGA’s employment guarantee to PM-KISAN’s farmer support and PAHAL’s subsidy delivery, DBT has revolutionized welfare schemes across sectors.

However, continued evolution and refinement remain essential to address persistent challenges including digital infrastructure gaps, literacy barriers, and vulnerable group access. The system’s COVID-19 response excellence proves its resilience, while innovations like e-RUPI demonstrate ongoing technological advancement.

As India advances toward becoming a $26 trillion economy, DBT’s role in ensuring inclusive growth, social justice, and efficient governance will remain fundamental. The system’s success provides a replicable model for developing nations seeking to modernize welfare delivery while maintaining fiscal discipline and social commitment.

+ There are no comments

Add yours