Key Highlights

- Constitutional Revenue Framework: Seventh Schedule Articles 245-246 divide legislative powers into Union List (100 subjects), State List (61 subjects), and Concurrent List (52 subjects) with specific taxation authorities for each level

- Finance Commission Devolution: 15th Finance Commission recommends 41% vertical devolution of central taxes to states for 2021-26 period, maintaining cooperative federalism while providing equitable resource distribution across states

- GST Compensation Mechanism: ₹7.61 trillion collected from July 2017 to July 2024 through compensation cess on luxury and sin goods, extended till March 2026 to repay pandemic loans and ensure state revenue protection

- Divisible Tax Pool Structure: Post-80th Amendment (2000), all central taxes except surcharges and specific cess form divisible pool, with current cess collections representing 23% of gross tax receipts remaining outside shared resources

- Multi-Stream Revenue Sources: Union derives income from customs, corporation tax, income tax, excise, GST, while states earn from SGST, alcohol excise, stamp duty, land revenue, vehicle tax, creating complementary revenue ecosystem

Constitutional Foundation: The Seventh Schedule Architecture

India’s federal revenue structure operates through a sophisticated constitutional framework established by the Seventh Schedule under Articles 245-246. This comprehensive system divides legislative powers—including taxation authority—into three distinct lists that form the backbone of India’s fiscal federalism. testbook

The Seventh Schedule creates constitutional certainty by clearly demarcating which level of government can tax what, eliminating jurisdictional conflicts while ensuring comprehensive coverage of all potential revenue sources. This systematic division has evolved over seven decades through constitutional amendments to adapt to changing economic realities.

Originally, the Union List contained 97 subjects, now expanded to 100 subjects, while the State List has been reduced from 66 to 61 subjects due to transfers to the Concurrent List. The Concurrent List has grown from 47 to 52 subjects, reflecting increasing areas requiring coordinated governance between Union and States.

Union Revenue Sources: National Taxation Powers

Primary Tax Revenue Streams

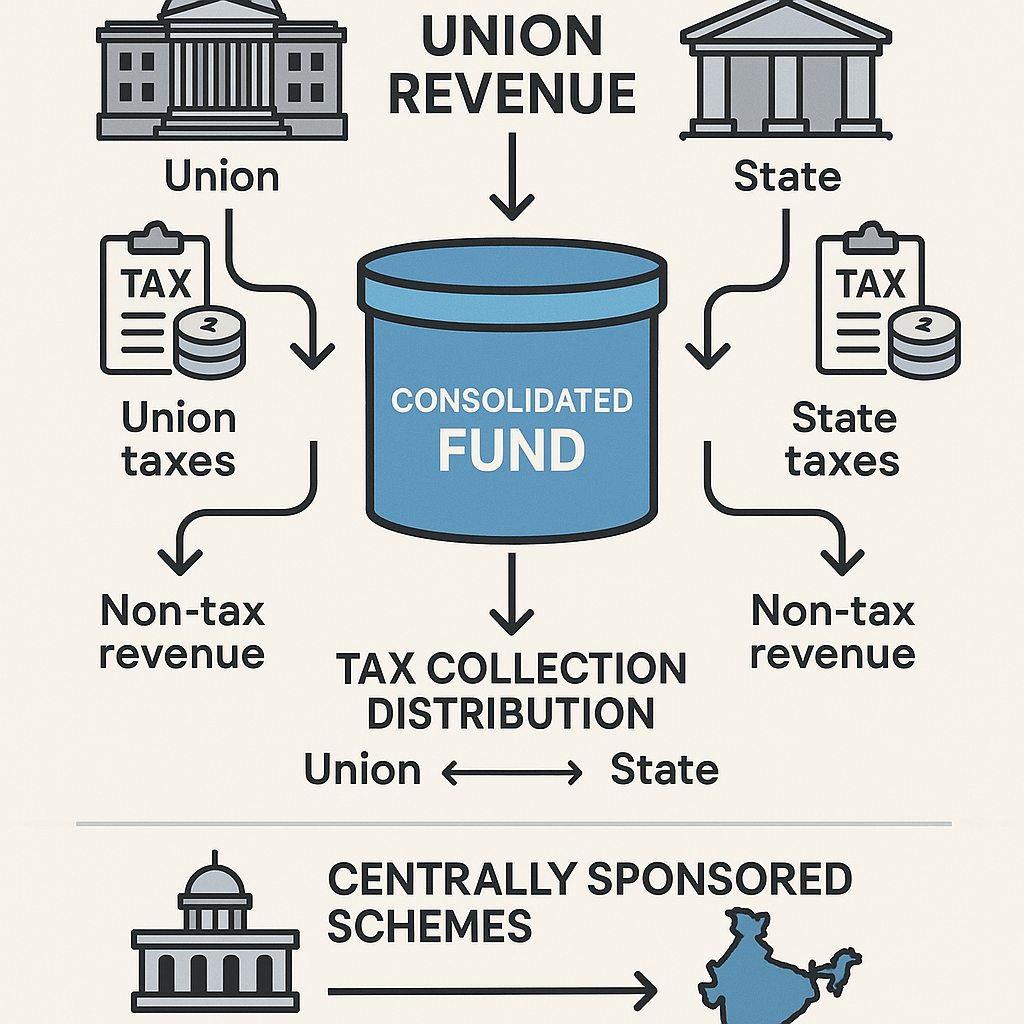

The Union Government derives its tax revenue from subjects listed in the Union List, focusing on matters of national importance that require uniform treatment across the country. Customs duties form the traditional backbone of central revenue, controlling international trade and protecting domestic industry. mea.gov

Corporation tax represents the largest single revenue source, with the Union having exclusive authority over company taxation. Income tax (excluding agricultural income) provides substantial revenue while enabling progressive taxation and wealth redistribution through federal transfers.

Goods and Services Tax (GST) has revolutionized the indirect tax landscape, with the Union collecting CGST while States collect SGST, creating a coordinated system that eliminates cascading effects. Excise duties on manufactured goods continue providing significant revenue despite GST subsumption of many items.

Non-Tax Revenue Contributions

Non-tax sources provide crucial supplementary revenue through dividends from Public Sector Undertakings (PSUs), profit transfers from RBI, and spectrum auction proceeds. Disinvestment receipts offer one-time revenue boosts while reducing government stake in commercial enterprises.

Union property revenue from railways, defense lands, and central government buildings provides steady income streams. Interest receipts on loans to states and foreign borrowings create additional revenue channels.

Petroleum and natural gas revenues through royalties and profit petroleum from offshore areas under Union jurisdiction contribute substantially to central finances.

State Revenue Autonomy: Regional Taxation Rights

Exclusive State Revenue Sources

State governments possess exclusive taxation authority over 61 subjects listed in the State List, focusing on regional and local matters requiring diverse approaches across different states. State Goods and Services Tax (SGST) forms the largest revenue source for most states post-2017.

Excise duties on alcohol provide significant revenue as states retain exclusive control over liquor taxation, with policies varying dramatically across states. Some states derive over 20% of revenue from alcohol excise, making it politically sensitive yet fiscally crucial.

Stamp duty on property transactions and legal documents provides stable revenue linked to real estate activity and economic growth. Land revenue though historically significant, now contributes minimally due to agricultural income exemptions and political considerations.

Vehicle taxation including registration fees, road tax, and permits creates growing revenue streams as automobile ownership expands. Electricity duty provides additional income while enabling cross-subsidization of agricultural and domestic consumers.

Agricultural and Natural Resource Revenue

Agricultural income tax remains exclusively with states, though most states have abolished or minimized such taxation for political reasons. Land revenue collection continues in modified forms through betterment levies and development charges.

Mineral royalties provide substantial revenue for mineral-rich states like Odisha, Jharkhand, and Chhattisgarh. Forest revenue through timber sales and non-timber forest products contributes to state finances while supporting conservation efforts.

Water charges and irrigation fees offer potential revenue sources though political considerations often limit collection effectiveness.

Finance Commission: The Devolution Architecture

Constitutional Mandate and Authority

Article 280 establishes the Finance Commission as a constitutional body responsible for recommending the distribution of tax revenues between the Union and States. Every five years, a new Finance Commission reviews fiscal arrangements and adjusts devolution formulas based on changing circumstances. indiabudget

The 15th Finance Commission, chaired by N.K. Singh, recommended 41% vertical devolution of shareable central taxes to states for 2021-26, representing a 1% reduction from the 14th Finance Commission’s 42% to accommodate Jammu & Kashmir and Ladakh as Union Territories.

Horizontal devolution among states follows sophisticated criteria: Income Distance (45% weightage) ensures poorer states receive larger shares, Demographic Performance (12.5% weightage) rewards population control efforts, and Forest & Ecology coverage recognizes environmental conservation.

Divisible Pool Evolution

The 80th Constitutional Amendment (2000) revolutionized tax sharing by creating a consolidated divisible pool of all central taxes except surcharges and cesses for specific purposes. This structural change simplified devolution while ensuring automatic sharing of tax buoyancy with states.

Current challenges arise from expanding cess collections—representing 23% of gross tax receipts—that remain outside the divisible pool, reducing states’ effective share of central revenue growth. States have repeatedly requested inclusion of cesses in the shareable pool.

Predictability in devolution enables better financial planning by states, though absolute amounts depend on central tax performance. Some states have requested guaranteed minimum amounts to ensure fiscal stability.

Grant Recommendations and Special Assistance

Article 280(3)(b) empowers the Finance Commission to recommend grants-in-aid for states assessed to be in need of assistance. These grants address specific developmental needs and fiscal imbalances beyond tax devolution.

Performance-based grants incentivize good governance, fiscal discipline, and achievement of developmental targets. Disaster relief funds provide additional support for calamity-affected states.

Local body grants recommended by Finance Commissions strengthen Panchayati Raj Institutions and Urban Local Bodies, promoting decentralized governance.

GST Compensation: Transitional Revenue Protection

Legal Framework and Implementation

The GST (Compensation to States) Act 2017 guaranteed states 14% annual revenue growth for five years (July 2017-June 2022) to address concerns about potential revenue losses from GST implementation. This constitutional assurance was crucial for securing state consensus on GST adoption. prsindia

Compensation cess levied on luxury and sin goods—including cigarettes, tobacco, pan masala, caffeinated beverages, coal, and premium vehicles—funds the compensation mechanism. Between July 2017 and July 2024, ₹7.61 trillion was collected through compensation cess.

COVID-19 pandemic created unprecedented revenue shortfalls, forcing the Centre to borrow and extend cess collection till March 2026 to repay loans taken for state compensation. This extension demonstrates federal commitment to fiscal partnerships.

Revenue Sharing Dynamics

GST architecture ensures equal stakeholding between Centre and States, with CGST and SGST collected equally on intra-state transactions, while IGST on inter-state trade is shared equally after destination-based settlement.

States’ protected revenue has grown at 14% CAGR since GST introduction, though cess collections have not kept pace with requirements, creating funding gaps during economic slowdowns. Current projections estimate compensation cess may need to continue beyond FY26.

Revenue implications of recent GST rationalization will test the sustainability of current compensation arrangements, as rate reductions may affect cess collections while states continue requiring support.

Centrally Sponsored Schemes: Cooperative Federalism

Cost-Sharing Mechanisms

Centrally Sponsored Schemes (CSS) represent cooperative federalism in action, with Union and State governments sharing costs for national priorities while respecting state autonomy. These schemes ensure uniform standards across states while leveraging combined resources. rrjournals

Funding patterns vary by scheme type: Core schemes typically follow 60:40 Centre-State cost sharing for general category states and 90:10 for northeastern and special category states. Optional schemes allow states to choose participation based on local priorities.

MGNREGA, Sarva Shiksha Abhiyan, National Health Mission, and other flagship programs demonstrate successful CSS implementation, combining central funding with state implementation and local adaptation.

Performance and Accountability

CSS design includes performance indicators, monitoring mechanisms, and outcome measurement to ensure effective utilization of shared resources. Digital platforms enable real-time tracking and transparent fund flow.

State flexibility in implementation allows adaptation to local conditions while maintaining national objectives. Capacity building components strengthen state institutions and human resources.

Evaluation studies regularly assess CSS effectiveness, leading to scheme modifications and improved design for better outcomes.

Revenue Challenges and Future Directions

Fiscal Imbalance Issues

Vertical fiscal imbalance—where states have greater expenditure responsibilities but limited revenue sources—creates structural dependence on central transfers. Expenditure assignments under Seventh Schedule often exceed revenue capacity at state level.

Horizontal imbalances among states vary significantly due to different resource endowments, development levels, and fiscal capacities. Finance Commission recommendations attempt to address these disparities through equalization transfers.

Off-budget borrowings and hidden liabilities in both Union and State finances create transparency concerns and fiscal risks. FRBM frameworks at both levels aim to ensure fiscal discipline.

Emerging Revenue Pressures

Digital economy creates new challenges for traditional tax bases, requiring innovative approaches to capture value creation in online platforms and digital services. Cryptocurrency and digital assets need regulatory frameworks for taxation.

Climate change and environmental degradation demand substantial investments in green infrastructure and adaptation measures, requiring additional revenue mobilization or resource reallocation.

Demographic transitions with aging populations and changing labor markets will impact tax bases and expenditure requirements, necessitating long-term fiscal planning.

Technology and Governance

Digital governance platforms improve tax administration, reduce compliance costs, and enhance transparency in revenue collection and transfer mechanisms. GST Network (GSTN) demonstrates successful technology deployment.

Data analytics enable better targeting of schemes and transfers, improving effectiveness while reducing leakages. Performance-based allocations become more feasible with real-time monitoring.

Blockchain technology and smart contracts could revolutionize inter-governmental transfers, ensuring automatic execution of devolution formulas and reducing administrative delays.

International Comparisons and Best Practices

Federal Finance Models

International experience in federal countries like Canada, Australia, Germany, and USA provides valuable insights for improving India’s fiscal federalism. Equalization mechanisms in these countries offer alternative approaches to addressing regional disparities.

Tax assignment principles and revenue sharing formulas vary across federal systems, with different emphasis on efficiency, equity, and autonomy. India’s model combines constitutional prescription with periodic review through Finance Commissions.

Borrowing constraints and fiscal responsibility frameworks in other federations provide lessons for managing subnational debt and ensuring fiscal sustainability.

Innovation in Revenue Mobilization

Environmental taxes, carbon pricing, and green bonds offer new revenue sources while promoting sustainable development. Several countries successfully integrate environmental objectives with fiscal policy.

Digital platforms for tax compliance and citizen services demonstrate potential for improving efficiency and reducing corruption. India’s JAM Trinity (Jan Dhan-Aadhaar-Mobile) provides foundation for enhanced service delivery.

Public-private partnerships in infrastructure and service delivery can leverage private resources while maintaining public control over essential services.

Conclusion

India’s federal revenue structure represents a sophisticated constitutional architecture that balances national unity with regional autonomy through systematic division of taxation powers and resource sharing mechanisms. The Seventh Schedule’s three-list system provides clarity and certainty while enabling evolution through constitutional amendments.

The Finance Commission framework under Article 280 ensures periodic review and adjustment of fiscal arrangements, maintaining relevance to changing economic conditions and developmental needs. The 15th Finance Commission’s 41% devolution reflects careful balancing of union and state requirements while accommodating new territorial arrangements.

GST implementation with its compensation mechanism demonstrates cooperative federalism in action, with Centre and States working together to manage transition challenges while protecting state interests. The ₹7.61 trillion compensation cess collection validates the importance of transitional support in major policy reforms.

Centrally Sponsored Schemes effectively combine central resources with state implementation, achieving national objectives while respecting federal principles. This partnership model enables coordinated development across diverse states with varying capacities.

Current challenges including growing cess collections outside the divisible pool, fiscal imbalances, and emerging economic patterns require continuous adaptation of revenue arrangements. Digital economy, environmental concerns, and demographic transitions will shape future fiscal federalism.

Technology integration offers unprecedented opportunities for improving efficiency, transparency, and service delivery in revenue administration and inter-governmental transfers. Digital platforms can strengthen accountability while reducing compliance costs.

The success of India’s federal finance system lies in its constitutional foundation combined with institutional flexibility through Finance Commissions and cooperative mechanisms like GST Council. This framework enables evolution while maintaining stability and federal harmony.

Future sustainability depends on addressing structural imbalances, expanding revenue bases, and adapting to emerging challenges while preserving the federal character that makes India’s diversity its strength. Continuous dialogue between Union and States through constitutional institutions will ensure that fiscal federalism continues serving India’s development aspirations.

+ There are no comments

Add yours