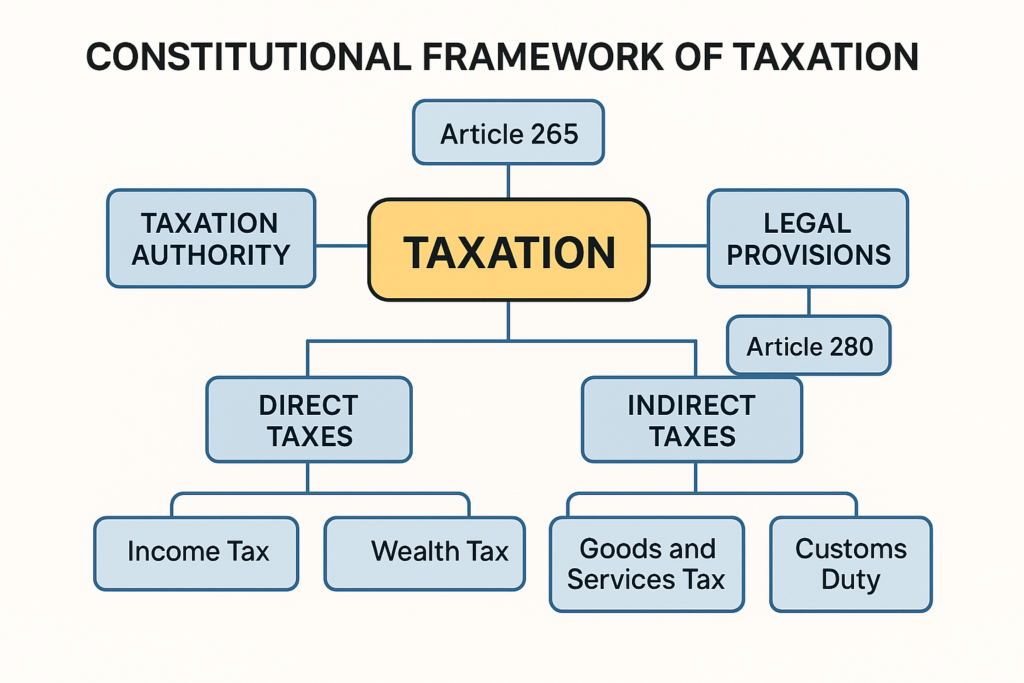

- Constitutional Foundation: Article 265 mandates “No tax shall be levied or collected except by authority of law,” ensuring legal basis for all taxation, while Article 280 establishes Finance Commission for Centre-State tax sharing recommendations

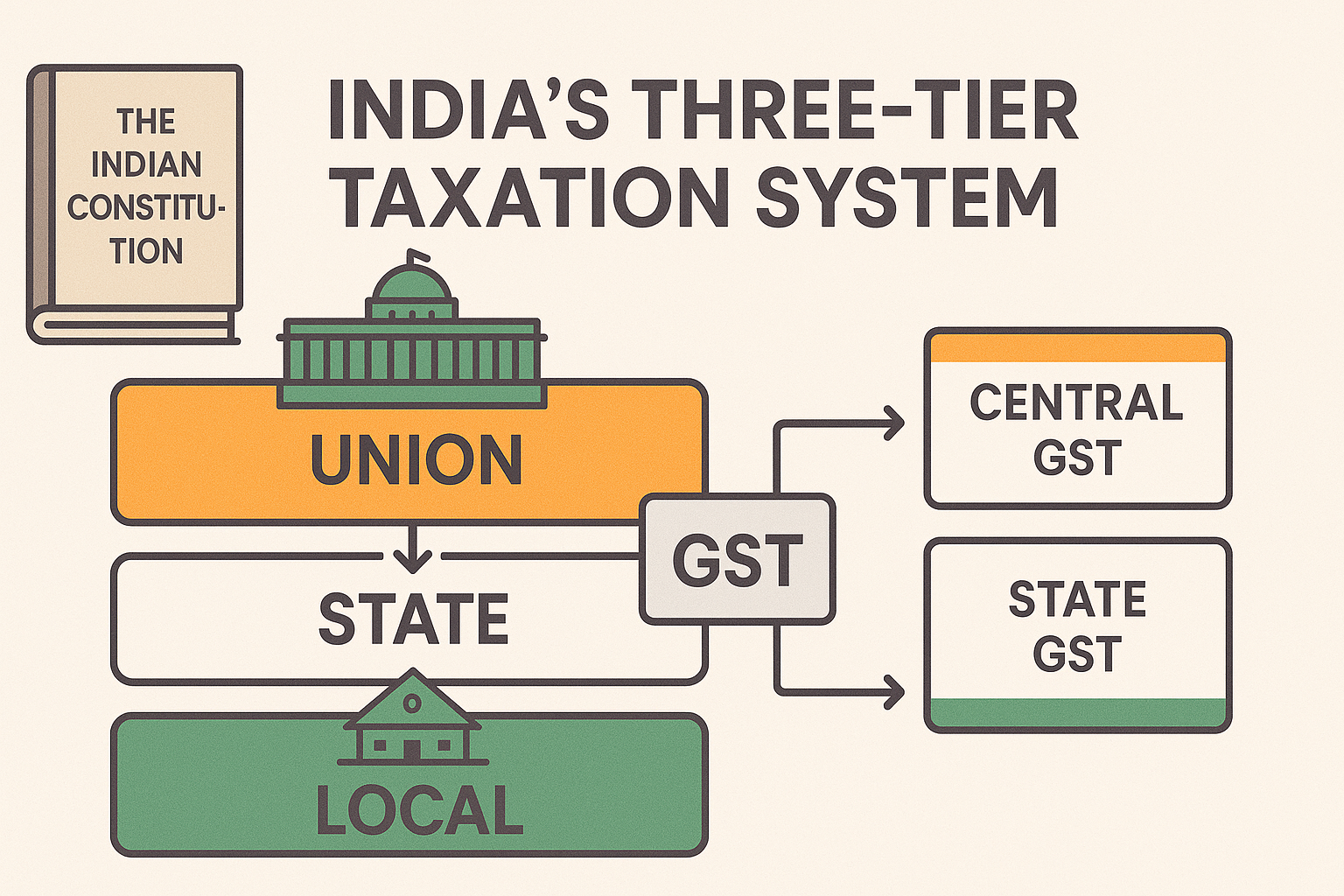

- Three-Tier Federal Structure: Union Government (List I), State Governments (List II), and Local Bodies have clearly demarcated taxation powers under 7th Schedule, with residuary tax powers vested in Centre

- Tax Classification System: Direct taxes (Income Tax, Corporate Tax) are borne by the payer and administered by CBDT, while indirect taxes (GST, Customs) are transferable to end consumers and managed by CBIC

- GST Revolutionary Reform: Launched July 1, 2017, GST subsumed 17 indirect taxes creating a unified market with CGST, SGST, IGST, UTGST structure, eliminating cascading effect and tax-on-tax

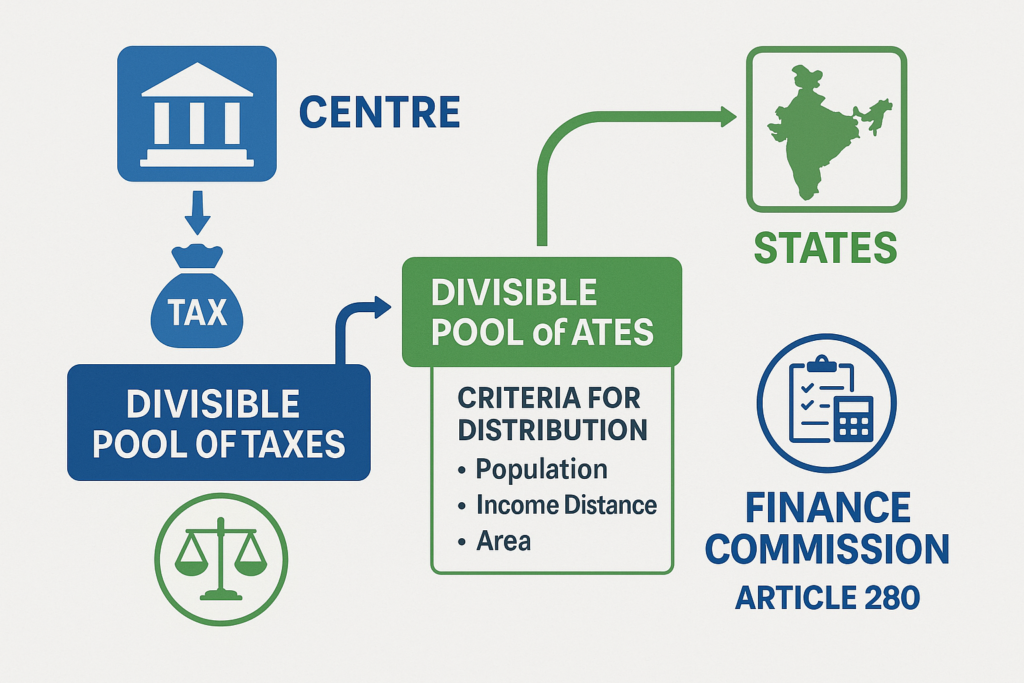

- Finance Commission Mandate: 15th Finance Commission increased States’ share in central tax proceeds from 32% to 41%, reflecting enhanced fiscal decentralization and cooperative federalism principles

Constitutional Architecture of Indian Taxation

India’s taxation system derives its authority from robust constitutional provisions that establish the legal framework for tax collection and distribution. The Constitution of India provides a comprehensive blueprint for fiscal federalism, ensuring balanced resource allocation between different levels of government.

Article 265 serves as the fundamental principle of Indian taxation, stating that “No tax shall be levied or collected except by authority of law”. This provision acts as a constitutional safeguard against arbitrary tax extraction and ensures that all taxation must have statutory backing through Acts of Parliament or State Legislatures. ipleaders

The landmark case Tangkhul v. Simirei Shailei established that even customary payments without legal authorization violate Article 265. The Court held that Rs. 50 daily payment to village headmen constituted unauthorized tax collection, reinforcing the constitutional requirement for legislative sanction.

Article 280 establishes the Finance Commission as a constitutional body responsible for recommending tax distribution between the Centre and States. The President constitutes a new Finance Commission every five years or at earlier intervals if necessary, ensuring regular review of fiscal arrangements. constitutionofindia.

Three-Tier Federal Structure: Division of Tax Powers

India’s federal tax architecture operates through a well-defined three-tier structure consisting of the Union Government, State Governments, and Local Bodies, each with distinct taxation powers outlined in the 7th Schedule of the Constitution. docs.manupatra

Union Government Tax Powers (List I)

The Union List contains tax subjects under Entries 82-92B, granting the Central Government authority over:

Income Tax (except agricultural income)

Corporation Tax on companies and corporate entities

Customs Duties on imports and exports

Central Excise on manufactured goods

Service Tax (now subsumed under GST)

Wealth Tax and Gift Tax (currently suspended)

Residuary powers under Entry 97 vest all unlisted tax matters with the Centre, providing flexibility for future tax innovations.

State Government Tax Powers (List II)

The State List enumerates state taxation authority under Entries 45-63, covering:

Agricultural Income Tax

Land Revenue and Property Tax

State Excise on liquor and narcotics

Motor Vehicle Tax and Road Tax

Entertainment Tax (partially subsumed under GST)

Stamp Duty on documents and transactions

Local Body Tax Powers

73rd and 74th Constitutional Amendments empowered Panchayati Raj Institutions and Urban Local Bodies with taxation authority for:

Property Tax collection and assessment

Professional Tax within prescribed limits

Water and Sewerage Charges

Market Fees and Octroi (where applicable

Finance Commission: Architect of Fiscal Federalism

The Finance Commission plays a pivotal role in India’s fiscal federalism by ensuring equitable distribution of tax revenues between the Centre and States. Article 280(3) mandates the Commission to make recommendations on: indiabudget

Tax Distribution Framework

Net proceeds distribution of shareable central taxes between Union and States

Allocation methodology among States for their respective shares

Principles governing grants-in-aid from the Consolidated Fund of India

Measures to augment State Consolidated Funds for Panchayat and Municipal resource supplementation

Evolution of Tax Sharing

The 80th Constitutional Amendment (2000) fundamentally altered tax sharing patterns by creating a consolidated divisible pool of all central taxes except surcharges and cesses for specific purposes. fincomindia

Recent trends show increasing devolution to States:

- 11th Finance Commission: 29.5% of central tax proceeds

- 14th Finance Commission: 42% of central tax proceeds

- 15th Finance Commission: 41% of central tax proceeds

This enhanced devolution reflects growing recognition of State fiscal needs and decentralization principles.

Direct vs. Indirect Tax Classification

India’s tax system is fundamentally divided into direct and indirect taxes, each serving distinct economic functions and administrative purposes. pkchopra

Direct Taxes: Personal Tax Burden

Direct taxes are levied directly on individuals and entities, with the tax burden falling on the actual taxpayer without possibility of transfer.

Key characteristics include:

- Progressive tax structure based on income slabs

- Non-transferable burden to other parties

- Administered by CBDT under Ministry of Finance

- Based on ability to pay principle

Major direct taxes comprise:

Income Tax: Individual and HUF taxation with exemption limit ₹2.5 lakh

Corporate Tax: Company taxation at 25-30% rates

Securities Transaction Tax (STT): On equity and derivative transactions

Dividend Distribution Tax (abolished from April 2020)

Indirect Taxes: Transferable Tax Burden

Indirect taxes are levied on goods and services with the tax burden ultimately transferred to end consumers.

Distinctive features include:

- Regressive nature affecting lower-income groups disproportionately

- Easy collection at production/sale points

- Administered by CBIC (Central Board of Indirect Taxes and Customs)

- Revenue buoyancy during economic growth

GST Revolution: Unifying India’s Indirect Tax System

The Goods and Services Tax (GST), implemented on July 1, 2017, represents India’s most ambitious tax reform since independence, fundamentally transforming the country’s indirect taxation landscape. eoiparis.gov

Pre-GST Fragmented System

Before GST, India’s indirect tax system was highly fragmented with multiple overlapping taxes:

Central taxes: Excise Duty, Service Tax, Additional Customs Duty, Special Additional Duty

State taxes: VAT, Central Sales Tax, Entry Tax, Luxury Tax, Entertainment Tax, Purchase Tax

Local taxes: Octroi, Local Body Tax

This complex structure created cascading effects (tax on tax), compliance burden, inter-state trade barriers, and significant tax evasion.

GST Structure and Design

GST adopts a four-tier structure designed to eliminate cascading and create a unified national market:

Central GST (CGST): Levied by Centre on intra-state supplies

State GST (SGST): Levied by States on intra-state supplies

Integrated GST (IGST): Levied by Centre on inter-state supplies

Union Territory GST (UTGST): Applicable in Union Territories

GST Rate Structure

The GST Council established multiple tax slabs for different categories:

0% (Nil rate): Essential items like milk, eggs, unprocessed food

5%: Basic necessities like edible oils, sugar, essential medicines

12%: Processed foods, smartphones, medical devices

18%: Standard rate for most goods and services

28%: Luxury items and sin goods like high-end cars, tobacco

Additional Cess: On luxury and sin goods over 28% rate

GST Impact and Benefits

Post-GST implementation demonstrated significant improvements:

Revenue growth: GST collections increased from ₹7.4 lakh crore (2017-18) to ₹18.07 lakh crore (2022-23)

Taxpayer base expansion: Registered taxpayers increased from 6.4 million to 14+ million

Compliance improvement: Return filing compliance above 95%

Ease of doing business: Single tax, online procedures, input tax credit

Economic Objectives of Taxation

India’s taxation system serves multiple economic objectives beyond revenue generation, contributing to macroeconomic stability and social equity.

Revenue Mobilization

Primary objective involves funding government expenditure on:

Public goods provision: Infrastructure, defense, law and order

Social services: Healthcare, education, poverty alleviation

Economic development: Industrial promotion, research and development

Debt servicing: Interest payments on government borrowings

Tax-to-GDP ratio in India stands at approximately 17-18%, indicating scope for enhancement compared to developed countries (25-30%).

Economic Regulation and Stabilization

Taxation serves as an important fiscal policy tool for:

Demand management: Counter-cyclical taxation during economic fluctuations

Inflation control: Higher tax rates during inflationary periods

Investment incentives: Tax holidays and deductions for priority sectors

Export promotion: Zero-rated supplies under GST for exporters

Income Redistribution and Social Equity

Progressive taxation contributes to reducing income inequality through:

Higher tax rates on wealthy individuals and corporations

Tax exemptions for lower-income groups

Subsidies funded through tax revenues

Social welfare schemes financed by tax collections

Contemporary Challenges and Reforms

Digital Economy Taxation

Emerging challenges include taxation of digital services, e-commerce transactions, and cryptocurrency. The government introduced:

Equalization Levy on digital advertising services

TDS provisions for e-commerce transactions

Crypto taxation framework with 1% TDS and 30% tax rate

Tax Administration Modernization

Technology adoption has transformed tax administration through:

Faceless assessment and appeals

Risk-based scrutiny selection

Data analytics for tax compliance monitoring

Digital payments and electronic filing

Cooperative Federalism Enhancement

GST Council model demonstrates successful cooperative federalism with:

Consensus-based decision making

Revenue sharing mechanisms

Joint administration of indirect taxes

Dispute resolution frameworks

Future Directions and Policy Implications

Tax Policy Reforms

Ongoing reforms focus on:

Direct tax code simplification

Corporate tax rate rationalization

Personal income tax structure optimization

International taxation alignment with global standards

Technology Integration

Future enhancements include:

Artificial Intelligence in tax compliance

Blockchain for tax transparency

Real-time tax monitoring systems

Integrated taxpayer services platforms

Conclusion

India’s three-tier taxation system represents a sophisticated federal structure that balances centralized coordination with decentralized autonomy. The constitutional framework established through Articles 265 and 280 provides robust foundations for legal taxation and equitable revenue distribution.

The GST revolution of 2017 transformed India’s fragmented indirect tax landscape into a unified national market, demonstrating the power of cooperative federalism and technology-enabled governance. The subsuming of 17 different taxes into four GST components eliminated cascading effects while enhancing revenue collection and compliance.

The Finance Commission’s evolving role in recommending increased devolution reflects India’s commitment to fiscal decentralization and empowerment of States. The enhancement from 32% to 41% devolution acknowledges States’ growing responsibilities in service delivery and development.

Direct and indirect tax classification serves distinct economic purposes, with progressive direct taxes ensuring equity while indirect taxes provide revenue buoyancy and administrative efficiency. The CBDT-CBIC administrative division ensures specialized expertise in different tax domains.

Contemporary challenges including digital economy taxation, international tax coordination, and compliance enhancement require continued policy innovation. The success of GST implementation provides confidence for future reforms including direct tax code and further digitization.

Technology integration through faceless procedures, data analytics, and real-time monitoring represents the future of tax administration. These innovations enhance both taxpayer convenience and revenue optimization while reducing compliance costs.

As India progresses toward becoming a developed economy, its taxation system must continue evolving to support growth objectives while maintaining fiscal sustainability. The constitutional framework provides sufficient flexibility for adaptation while preserving federal balance and democratic accountability.

The success of India’s taxation system lies in its ability to balance revenue generation, economic regulation, and social equity within a complex federal structure. Continued reforms focusing on simplification, technology adoption, and cooperative federalism will ensure sustainability of this critical governance institution.

+ There are no comments

Add yours