Key Highlights:

- India processes 20+ billion UPI transactions monthly (August 2025), making it a global leader in real-time digital payments with $1.5 trillion in annual digital transactions

- Only 40% of SC/ST and 36% of women use mobile/internet banking compared to 80% among general caste respondents, revealing a stark digital divide

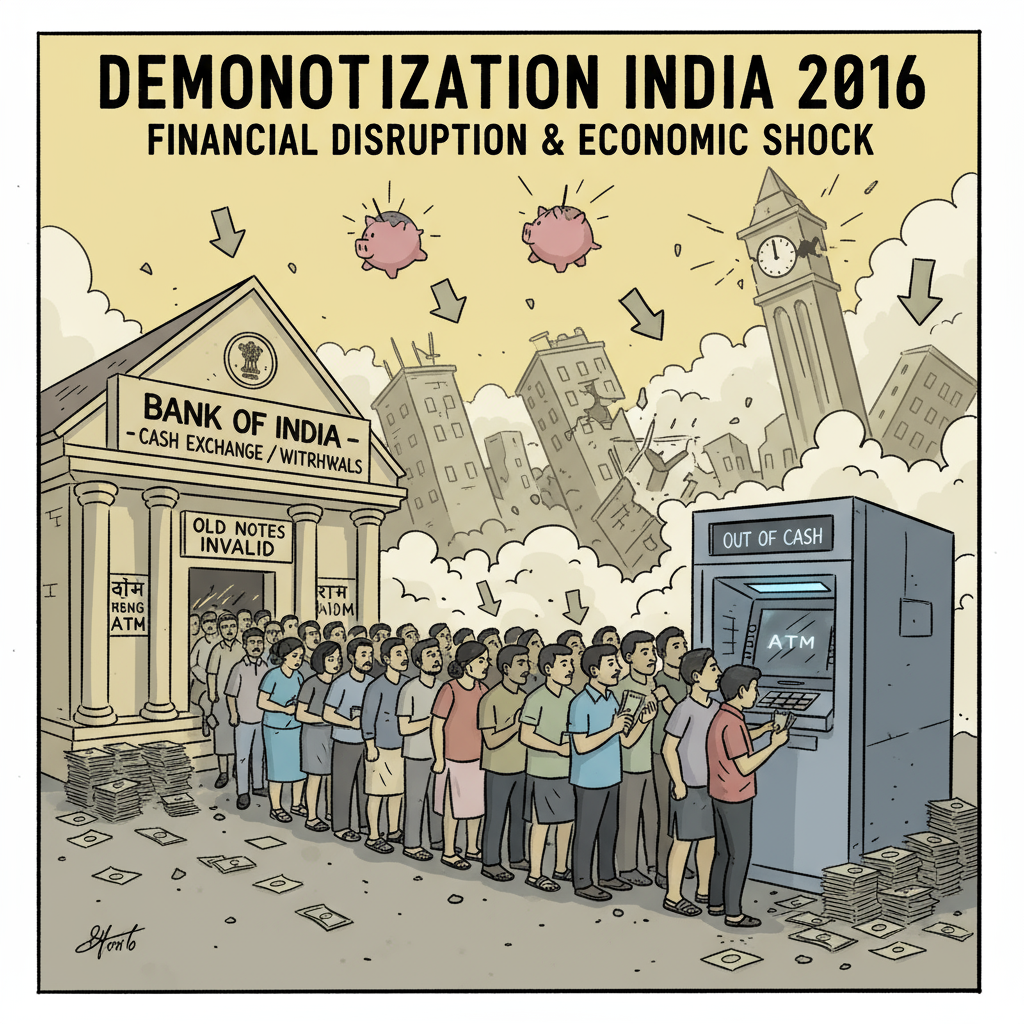

- Demonetization 2016 withdrew 86% of India’s currency overnight, forcing digital adoption but causing massive disruption, especially for the poor and marginalized

- 52+ crore Jan Dhan accounts opened under PMJDY, but significant portions remain dormant, indicating access without meaningful usage

- Financial Secretary M. Nagaraju acknowledges rural connectivity and tribal access remain major challenges despite UPI’s substantial growth

The Two Faces of India’s Digital Payment Boom

India stands at a fascinating crossroads. With over 20 billion UPI transactions monthly and $1.5 trillion in annual digital payments, the country has emerged as a global fintech powerhouse. The government’s ambitious vision—transitioning from a cash-dependent economy to a “faceless, paperless, cashless” society—has driven initiatives like the JAM Trinity (Jan Dhan-Aadhaar-Mobile), demonetization, and the Digital India mission. ibef

Yet beneath these impressive statistics lies a critical debate: Is India’s digital revolution a story of voluntary empowerment or forced exclusion?

The question is not merely academic. It touches upon fundamental issues of financial inclusion, equity, technology governance, and socio-economic justice. As India races toward digitalization, millions of rural poor, elderly citizens, women, and marginalized communities risk being left behind—creating what researchers call the “new digital divide”.

This comprehensive analysis examines both sides of India’s cashless transformation, backed by research data and real-world evidence.

India’s Digital Payment Infrastructure: The Building Blocks

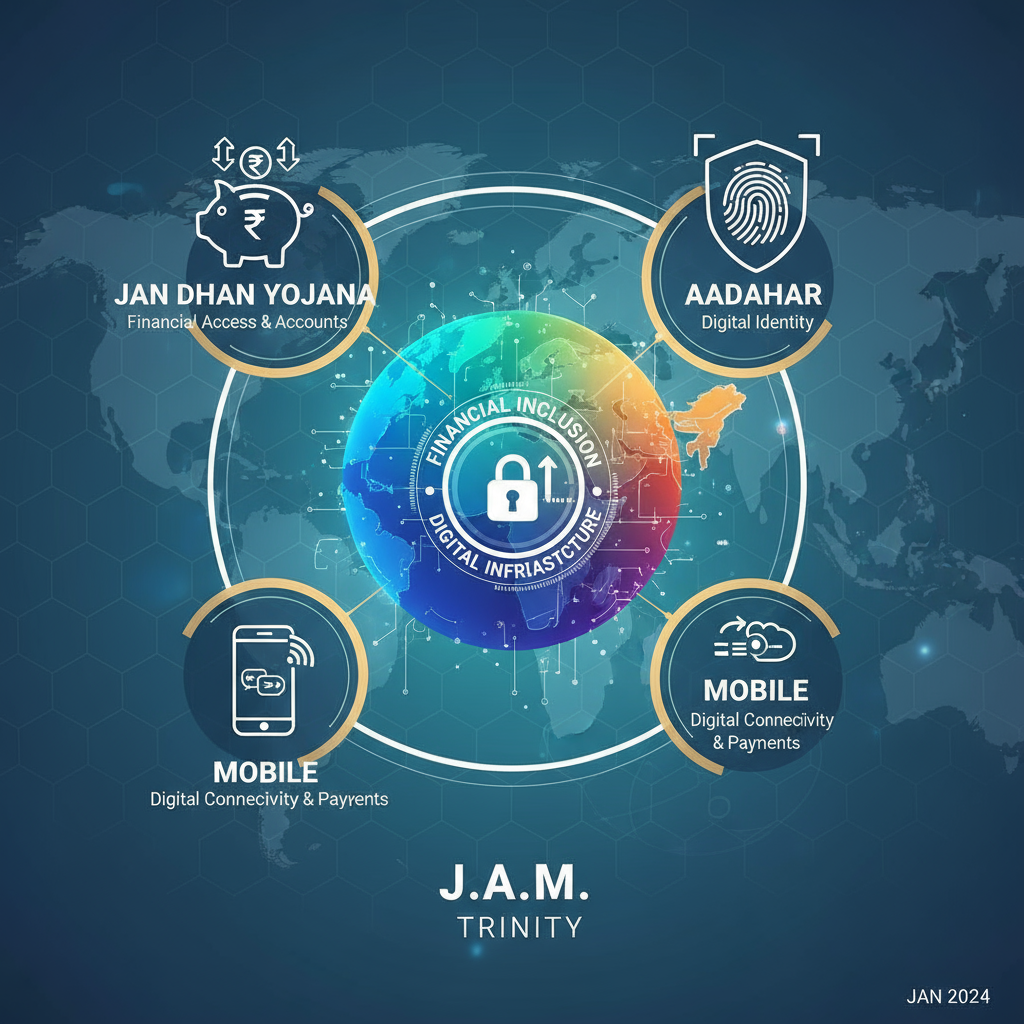

The JAM Trinity: Foundation of Digital Finance

India’s digital payment ecosystem rests on three interconnected pillars:

Jan Dhan (Bank Accounts): The Pradhan Mantri Jan Dhan Yojana (PMJDY), launched in 2014, has opened over 52 crore bank accounts, bringing previously unbanked populations into the formal financial system. As of August 2024, these accounts hold deposits worth ₹2.30 lakh crore ($27.51 billion). pib.gov

Aadhaar (Digital Identity): Biometric digital identity enables seamless e-KYC verification and direct benefit transfers, eliminating intermediaries and reducing leakages.

Mobile (Connectivity): Increasing smartphone penetration facilitates mobile banking and UPI access, creating the technological backbone for digital transactions.

UPI: The Crown Jewel of India’s Digital Payments

Launched in 2016 by the National Payments Corporation of India (NPCI) under RBI’s guidance, the Unified Payments Interface has transformed how India transacts.

Key Statistics:

- August 2025: UPI crossed 20 billion monthly transactions for the first time, processing ₹24.85 lakh crore ($281 billion)

- Daily Average: 645 million transactions per day

- Growth Trajectory: 34% year-on-year volume growth and 21% value growth

- Market Dominance: UPI accounts for 85% of India’s digital payment transactions

- Zero MDR Policy: No Merchant Discount Rate charges encourage widespread adoption

Why UPI Succeeded:

- Real-time interbank payment system with instant settlements

- Interoperability across banks, wallets, and platforms

- Simple QR code-based payments accessible to merchants of all sizes

- Government backing and zero transaction fees for merchants

Government Initiatives: Pushing the Cashless Agenda

Demonetization: The Shock Therapy of 2016

On November 8, 2016, Prime Minister Narendra Modi announced the sudden withdrawal of ₹500 and ₹1,000 notes—representing 86% of currency in circulation.

Stated Objectives:

- Curb black money and corruption

- Combat counterfeit currency and terrorism financing

- Accelerate India’s transition to a digital, cashless economy

Immediate Impact:

- Prolonged cash shortages causing massive economic disruption

- Long queues at banks and ATMs; multiple deaths reported

- Forced overnight shift to digital payments without adequate preparation ijrbs

Mixed Results:

- 99.3% of demonetized notes returned to banks, suggesting failure to eliminate black money

- GDP growth rate declined; an estimated 1.5 million jobs lost

- Informal economy severely hit—which accounts for 82% of employment and nearly half of GDP

- Digital payment adoption surged, but at significant human and economic cost

Financial Inclusion Schemes

PMJDY Benefits:

- RuPay debit cards with ₹2 lakh accident insurance

- Direct Benefit Transfer (DBT) eliminating intermediaries and reducing leakages

- Micro-insurance, overdraft facilities, and pension schemes accessible digitally

- Jan Dhan Darshak App mapping over 1.3 million banking touchpoints

Digital India Initiative:

- “Faceless, Paperless, Cashless” vision driving government services online

- Infrastructure expansion for digital payments

- Goal: Transform India into a digitally empowered knowledge economy

The Critical Debate: Inclusion or Exclusion?

Arguments for Financial Inclusion

Positive Impacts:

Access to Formal Economy: Over 520 million previously unbanked individuals now have bank accounts, integrating them into the financial mainstream.

Convenience and Efficiency: Instant fund transfers, 24×7 availability, reduced transaction costs, and elimination of physical cash handling.

Transparency and Governance: Digital trails reduce corruption, enable better tax collection, and improve welfare delivery. The government saved approximately ₹3.48 lakh crore in leakages through DBT enabled by Jan Dhan accounts.

Economic Empowerment: Women accessing banking independently; entrepreneurship enablement through digital credit and payments.

COVID-19 Catalyst: The pandemic demonstrated the necessity of digital alternatives when physical transactions became risky.

Arguments Against Forced Digitalization

The Digital Divide:

Research from Kolhapur district, Maharashtra, reveals stark disparities:

- Only 40% of SC/ST respondents use mobile/internet banking compared to 80% among general caste respondents

- Only 36% of women use digital banking services

- Age discrimination: Elderly populations struggling with digital interfaces, dependent on intermediaries

Infrastructure Deficits:

Financial Secretary M. Nagaraju candidly acknowledged in October 2025: “UPI growth has been very substantial, but one challenge we have is bringing entire communities living in tribal and rural areas into a formal financial system. At many places, we also have the challenge of the internet. Therefore, offline transactions and rural transactions are our challenge”.

Key infrastructure barriers include:

- 60% of rural areas face poor internet connectivity

- Only 3.8% of rural households have fiber internet vs. 15.3% urban

- Twice as many rural households (16.7%) lack internet access compared to urban (8.4%)

- Power outages disrupting digital transactions

- Biometric failures at Customer Service Points (CSPs) and AePS glitches

Financial Literacy Gap:

The 246-respondent NCR study found high account ownership but low usage among vulnerable groups. Many Jan Dhan accounts remain dormant—lacking understanding of digital products and services.

Key Barriers:

- Language barriers: India’s 120+ languages mean many don’t speak major FinTech languages

- Low confidence and digital illiteracy

- Fear of fraud and cybersecurity concerns

Coercive Elements:

Demonetization’s overnight cash withdrawal forced digitalization without preparedness. Increasing government subsidies and welfare schemes are digital-only, creating compulsion rather than choice. Cash transactions face stigmatization; digital promoted as morally superior.

Socio-Economic Impacts: Winners and Losers

The New Digital Divide

Traditional financial exclusion meant lack of bank accounts. The new digital divide means having accounts but being unable or unwilling to use digital services.

Two-Tier System Emerging:

- Digitally included: Urban, educated, affluent individuals transacting seamlessly

- Digitally excluded: Rural, elderly, women, lower castes relying on cash, facing discrimination

Dormant Accounts Crisis:

Despite 52+ crore Jan Dhan accounts opened, significant challenges persist:

- 26% of Jan Dhan accounts with PSBs are inactive as of September 2025

- 35% of bank account holders in India became inactive by 2021 (World Bank Global Findex Report)

- 11 crore inactive accounts as of December 2024

- Accounts serve only for DBT receipt, not financial empowerment

Reasons for Inactivity:

- Banks too remote (28% of dormant account holders), particularly in rural areas

- Lack of trust in financial institutions

- No perceived need for active account usage

- Digital illiteracy and confidence gaps

Gender Disparity

Women face multiple barriers to digital financial inclusion:

- Lower smartphone ownership and mobile internet access (33% less likely than men)

- Limited digital literacy (only 35% aware of digital financial services)

- Cultural restrictions on digital engagement

- Preference for cash due to trust deficit

Women’s World Banking research highlights that over 200 million Indian women are poised to adopt digital payments if provided with right support and education. Connectivity issues and limited literacy, especially among women, create barriers reinforcing cash dependence.

Caste-Based Digital Inequality

Digital divide closely mirrors India’s social stratification:

- Only 8% of General caste have computers/laptops

- Less than 1% of ST and 2% of SC have access to computers

- Internet access: 92% of dominant caste urban households vs. 71% of ST households

- Digital banking adoption negatively correlated with SC/ST status

Comparative Global Perspectives

India Stack vs. Kenya’s M-Pesa vs. Brazil’s Pix

India Stack (Government-Led):

- Approach: Government creating digital infrastructure (Aadhaar, UPI) as public good

- Strengths: Rapid scale, interoperability, zero MDR enabling widespread adoption thedocs.worldbank

- Weaknesses: Market distortions, privacy concerns, forced adoption, crowding out private innovation

Kenya’s M-Pesa (Private-Sector Led):

- Launched 2007 by telecom company Safaricom in partnership with Commercial Bank of Africa

- Success: Expanded financial inclusion from 26% (2006) to 84% (2021); lifted hundreds of thousands out of poverty

- Market-driven: Private sector identifying opportunities, implementing culturally appropriate solutions

- 51+ million users, $314 billion in annual transactions across multiple African countries

Brazil’s Pix (Central Bank-Led):

- Launched 2020 by Brazil’s Central Bank (BCB) as fast-payment system similar to UPI

- Rapid growth: 1.2 million transactions monthly in 2021; exponential expansion since

- 85% population access to financial services; used for social programs like Bolsa Familia

- More centralized than India Stack—BCB both owns and operates the payment scheme

Comparative Lesson:

Research comparing these systems reveals that private digital platform providers (M-Pesa, Yape in Peru) led to more robust and user-friendly payment solutions than government-led systems (UPI, Pix) where central banks took the leading role.

Key Insight: Government should provide genuine public goods (identity verification, regulatory framework) while avoiding direct competition with private players, which can inhibit innovation. Market actors are better positioned for context-specific, user-friendly digital payment solutions.

Challenges to Inclusive Cashless Economy

Technological Barriers

- Poor internet connectivity in 60% rural areas

- Limited smartphone penetration among low-income groups

- Technical glitches and system downtimes eroding trust

Socio-Cultural Factors

- Cash deeply embedded in Indian culture; psychological attachment

- Distrust of formal financial systems among marginalized communities

- Preference for tangible, visible money, especially among poor and elderly

Institutional Deficits

- Lack of grievance redressal mechanisms for digital payment issues

- Insufficient customer support in vernacular languages

- Coordination gaps between multiple regulators (RBI, TRAI, MeitY, NITI Aayog)

Security and Privacy Concerns

- Rising cybersecurity threats: phishing, malware, SIM swaps, social engineering

- Aadhaar data leaks raising alarm about privacy violations

- Lack of consumer awareness about safe digital practices

Zero MDR Sustainability Challenge

The zero Merchant Discount Rate (MDR) policy challenges long-term sustainability of UPI ecosystem:

- Favors tech giants (Google Pay, PhonePe, Walmart) over traditional banks and payment networks

- Companies monetize through data, advertising, and e-commerce rather than transaction fees

- Private sector innovation potentially crowded out by subsidized government platforms

- Government provides annual budgetary allocations to incentivize banks and payment providers

Financial Secretary Nagaraju clarified in October 2025: “The government has only said we are not imposing MDR charges”.

Policy Recommendations: Toward Inclusive Digitalization

1. Ensuring Voluntariness, Not Coercion

- Maintain cash as legal tender; prohibit merchant refusal of cash

- Digital should complement, not replace cash

- Avoid overnight shocks like demonetization

2. Bridging the Digital Divide

Infrastructure Development:

- Universal broadband connectivity; accelerate BharatNet Phase III

- Subsidized smartphones for Below Poverty Line (BPL) families

- Offline digital payment solutions: RBI’s eRupee CBDC with offline capabilities being piloted

Digital Literacy:

- Mass campaigns in vernacular languages

- Financial and digital literacy integrated into school curricula

- Community-based training focusing on women, elderly, SC/ST populations

3. Strengthening Consumer Protection

Security Measures:

- AI-powered fraud detection and real-time alerts

- Mandatory two-factor authentication and transaction limits

- Cybersecurity awareness campaigns

Grievance Redressal:

- 24×7 helplines in multiple languages

- Ombudsman for digital payments; fast-track dispute resolution

- Liability protection for genuine fraud victims

4. Data Privacy and Governance

- Strict implementation of Digital Personal Data Protection Act, 2023

- Minimize Aadhaar linkage; purpose limitation and data minimization principles

- User control over data sharing; transparency in data usage

5. Regulatory Reforms

Level Playing Field:

- Rational MDR policy balancing stakeholder interests

- Remove discriminatory barriers (AePS access restrictions, user limits)

- Support both public and private innovation

Coordination:

- Unified regulator or coordination mechanism among RBI, TRAI, MeitY

- Consistent, predictable regulations fostering innovation

6. Social Inclusion Measures

Targeted Interventions:

- UPI for Her initiative: Women-focused digital literacy collaboration between NPCI and Women’s World Banking

- SC/ST-specific capacity building addressing caste-based digital divide

- Elderly-friendly interfaces: voice-based, vernacular UX

Accessible Design:

7. Monitoring and Evaluation

- Periodic assessments of financial inclusion and digital divide indicators

- Disaggregated data (gender, caste, age, geography) tracking exclusion

- Course correction based on evidence, not ideology

Way Forward: Balancing Innovation and Inclusion

Short-Term (1-2 years)

- Launch comprehensive digital-financial literacy campaign targeting 50 crore adults

- Expand BharatNet to all gram panchayats; ensure 4G connectivity

- Pilot eRupee with offline capabilities in 100 districts

- Strengthen cybersecurity; establish digital payments ombudsman

Medium-Term (3-5 years)

- Achieve 100% digital literacy among 18-60 age group

- Ensure 90% rural India has reliable internet and smartphone access

- Transition to sustainable MDR model supporting all stakeholders

- Integrate cash and digital seamlessly; no forced digitalization

Long-Term (5-10 years)

- Position India as model for inclusive digital finance globally

- Cashless by choice, not compulsion; empowered, not excluded citizens

- Export India Stack responsibly to developing countries, learning from implementation challenges

Conclusion: The Road Ahead

India’s digital payment revolution is undeniably remarkable—20+ billion UPI transactions monthly, $1.5 trillion digital economy, and global leadership in real-time payments. Government initiatives like JAM Trinity, demonetization, zero MDR policy, and Digital India have driven unprecedented adoption.

Yet the critical question persists: Is this voluntary empowerment or forced exclusion?

The evidence points to a new digital divide—where 40% SC/ST, 36% women, elderly, and rural populations remain excluded despite having bank accounts. Infrastructure gaps, digital illiteracy, privacy concerns, security threats, and market distortions create significant challenges.

Coercive elements—demonetization’s overnight shock, cash stigmatization, welfare digitalization—have compelled adoption rather than enabling genuine choice.

Winners: Tech giants (Google Pay, PhonePe, Paytm), urban educated users, government (enhanced tax collection, reduced leakages).

Losers: Rural poor, marginalized communities, small merchants, elderly, privacy advocates—those least able to adapt bearing the heaviest burden.

The Path Forward:

The imperative is clear: Financial inclusion requires meeting people where they are—cash or digital—empowering choice, not imposing it.

As Financial Secretary M. Nagaraju acknowledged, bringing tribal and rural communities into the formal financial system remains a major challenge despite UPI’s growth. Women’s World Banking research reveals that connectivity issues and limited literacy, especially among women, create barriers reinforcing cash dependence.

True financial inclusion demands:

- Voluntariness over coercion

- Infrastructure bridging digital divides

- Vernacular digital literacy

- Consumer protection and data privacy

- Regulatory reforms creating level playing fields

- Social inclusion measures addressing caste, gender, and age disparities

- Evidence-based monitoring and course correction

The Ultimate Vision:

An India where digital finance enhances, not replaces; includes, not excludes; empowers, not coerces. Cashless India should be an aspiration achieved through persuasion, capability-building, and trust—not a forced march leaving the vulnerable behind.

Digital payments are a powerful tool for inclusion IF accompanied by infrastructure, literacy, genuine choice, and robust protection. The challenge is ensuring that India’s remarkable technological progress translates into equitable prosperity for all citizens—not just the digitally privileged few.

+ There are no comments

Add yours