Key Highlights:

- 512 billion SHIB tokens worth ₹63.4 crore transferred from Kraken hot wallet to anonymous address, making recipient the 38th largest Shiba Inu holder and signaling long-term bullish sentiment

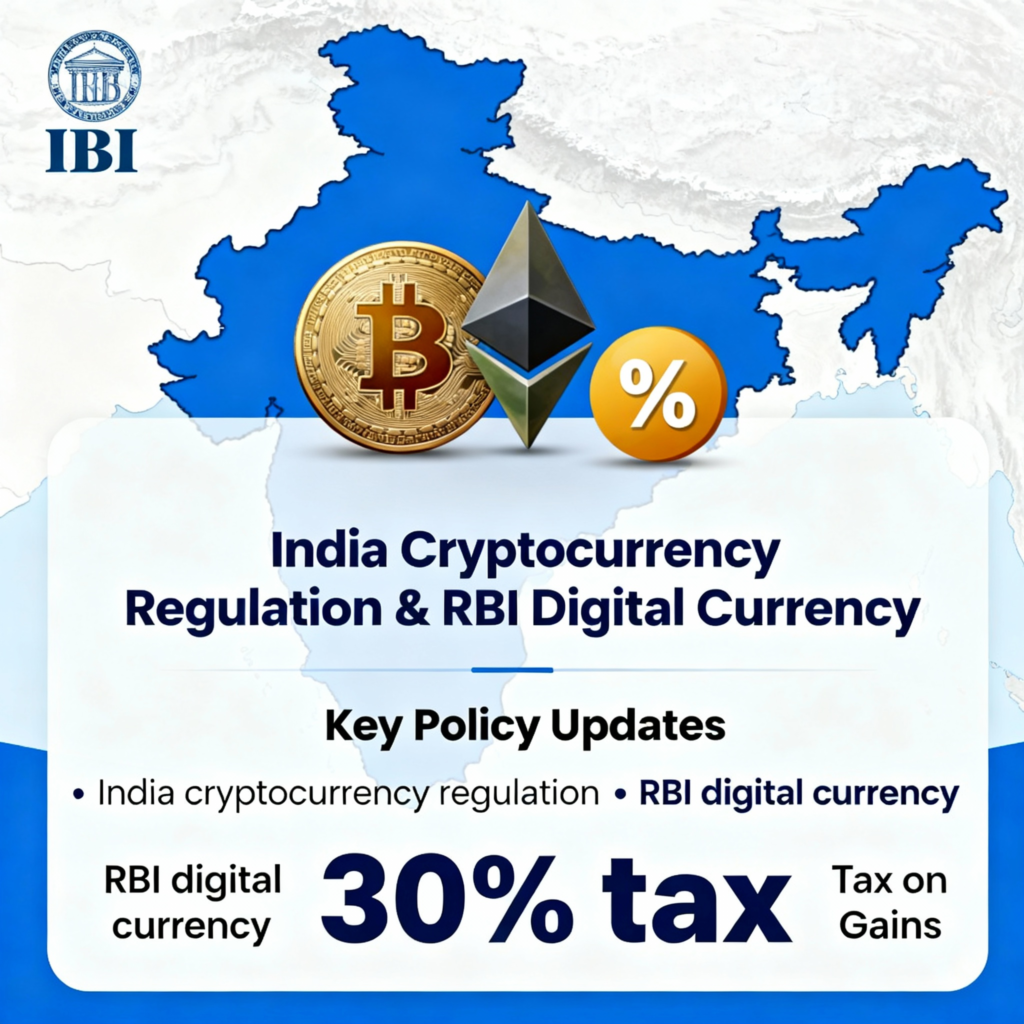

- India imposes 30% flat tax on crypto gains plus 1% TDS on transactions exceeding ₹50,000, while discouraging non-asset-backed cryptocurrencies through heavy taxation policies

- Meme coin market projected to grow from $68.5 billion in 2024 to $925.2 billion by 2035 at 26.7% CAGR, driven by community engagement and whale activity dynamics

- RBI plans state-backed digital currency while maintaining cautious stance on private cryptocurrencies, citing financial stability and sovereignty concerns for regulatory framework

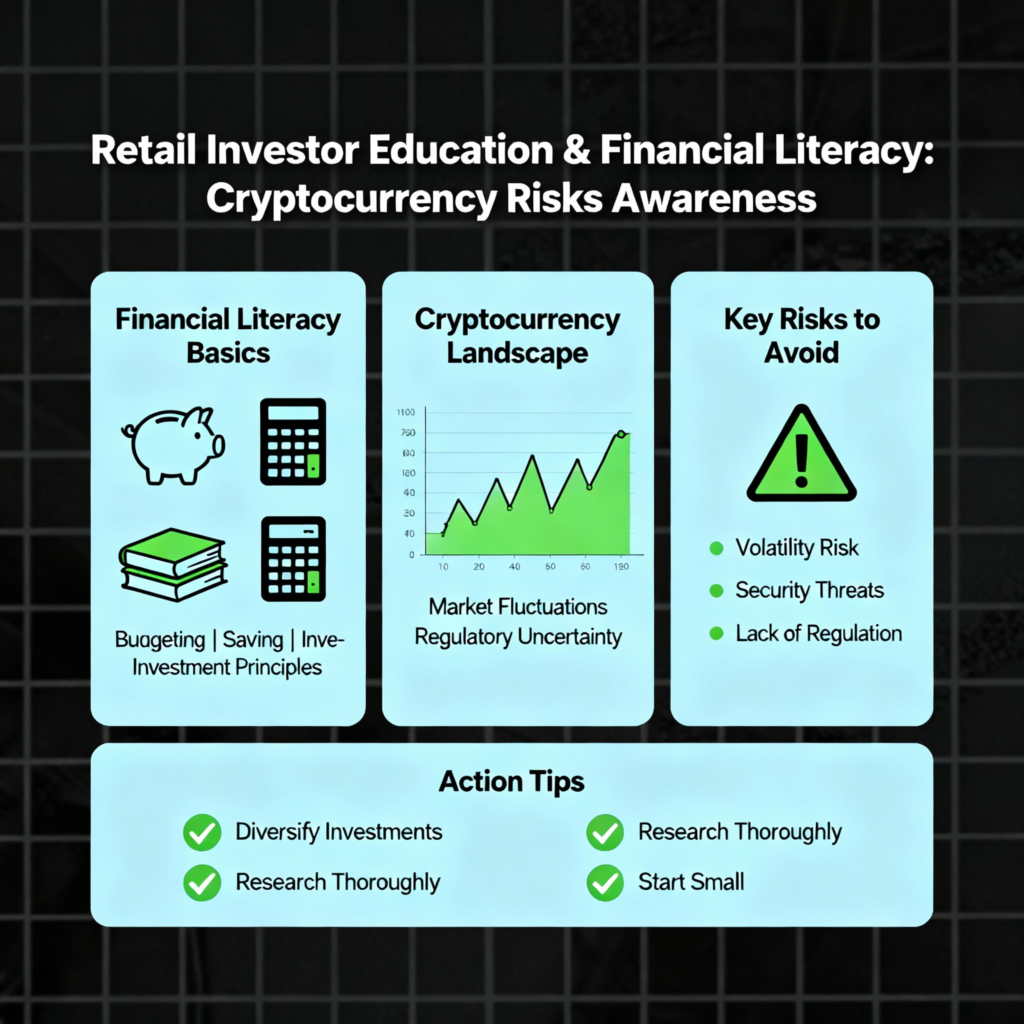

- Whale manipulation remains critical risk with coordinated buying and dumping schemes affecting retail investors, requiring enhanced on-chain analytics and investor education programs

The Meme Coin Revolution Meets Regulatory Reality

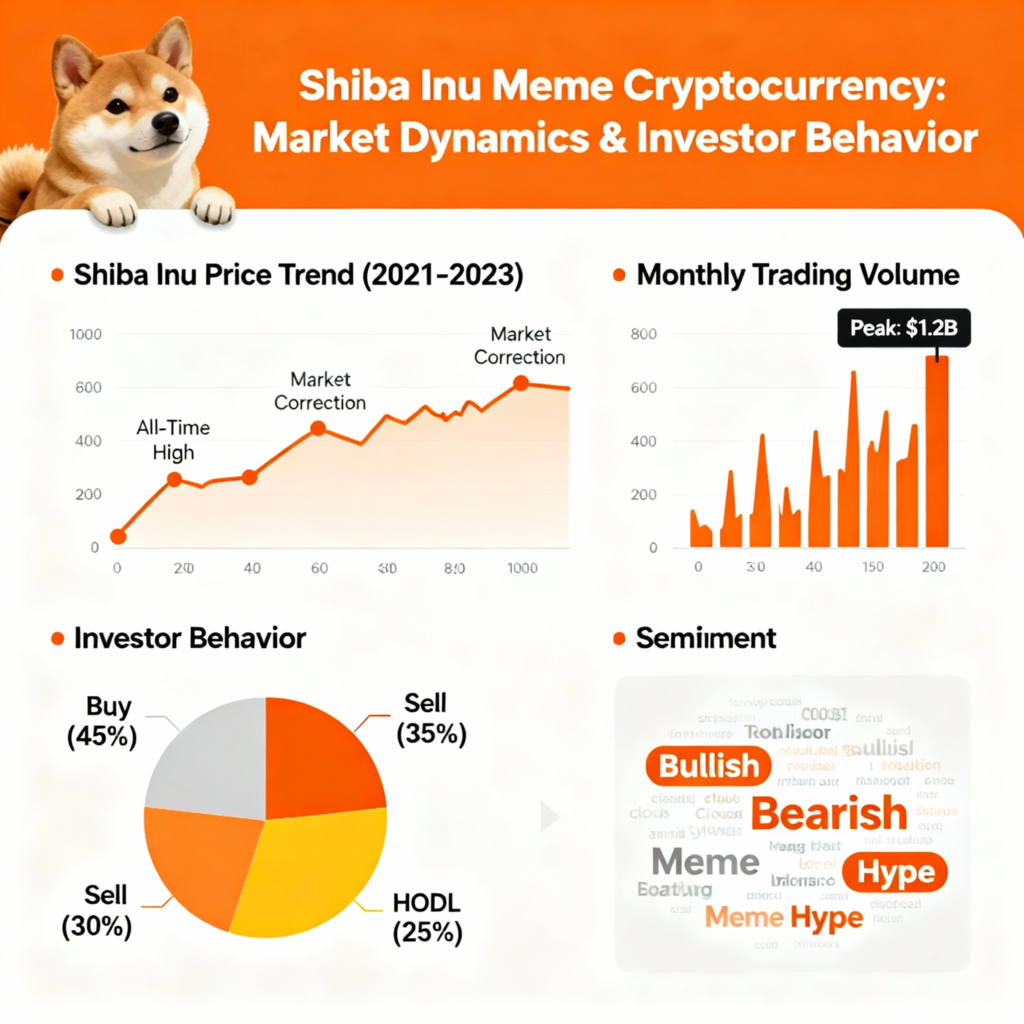

The cryptocurrency landscape witnessed a seismic shift when 512 billion Shiba Inu (SHIB) tokens worth approximately ₹63.4 crore ($7.14 million) were transferred from a Kraken hot wallet to an anonymous address. This massive transaction, representing one of the largest SHIB movements in recent months, has instantly catapulted the recipient into the ranks of the 38th largest Shiba Inu holder globally. binance

The timing is particularly significant: this accumulation occurred during a 5% daily price decline for SHIB, suggesting contrarian investment behavior typical of sophisticated institutional players rather than panic-driven retail trading. The transaction demonstrates growing confidence in long-term meme coin value despite current market volatility and regulatory uncertainties.

With India’s evolving cryptocurrency stance – including 30% taxation on crypto gains and plans for an RBI-backed digital currency – understanding these dynamics becomes essential for evidence-based governance in the digital age.

The broader context is equally compelling: the global meme coin market is projected to expand from $68.5 billion in 2024 to $925.2 billion by 2035, representing a compound annual growth rate of 26.7%. This explosive growth trajectory raises fundamental questions about financial stability, investor protection, and regulatory adaptation in rapidly evolving digital asset ecosystems. metatechinsights

Market Dynamics and Whale Behavior: Decoding the 512 Billion SHIB Transfer

Analyzing Transaction Patterns and Long-Term Sentiment

The 512 billion SHIB transfer represents a classic “hot-to-cold” wallet movement, indicating strategic long-term positioning rather than speculative trading. Etherscan data confirms the tokens moved from Kraken’s hot wallet (used for active trading) to address 0x95a…4C4cE, which security analysts believe may be Kraken’s cold storage facility for long-term asset preservation. binance

Post-transfer analysis reveals continued accumulation:

- Initial deposit: 512 billion SHIB tokens

- Current balance: 1.47 trillion SHIB tokens (₹171 crore value)

- Additional purchases: Nearly 1 trillion tokens acquired since initial transfer

- Strategy confirmation: Consistent accumulation during price weakness

Whale Influence on Market Dynamics

Cryptocurrency whales wield disproportionate influence over meme coin markets through coordinated strategies that can dramatically impact prices:

Accumulation Phase Tactics:

- Strategic buying during market downturns to acquire large positions at attractive prices

- Off-exchange transactions to minimize immediate market impact

- Cold storage transfers signaling long-term commitment to retail investors

Market Impact Mechanisms:

- Supply reduction through large-scale accumulation creating artificial scarcity

- Sentiment manipulation as retail investors interpret whale movements as bullish signals

- Liquidity constraints when significant token supplies are removed from active trading

The PEPE Success Case Study:

Recent analysis reveals a whale who invested $200,000 in PEPE coins achieved $1.77 million profit (886% return) within nine months, demonstrating the potential for sophisticated meme coin strategies. This success story amplifies retail interest and validates whale accumulation strategies across the meme coin ecosystem. onesafe

Social Media and Community-Driven Valuation

Meme coins uniquely depend on social sentiment and community engagement for value creation, differentiating them from traditional cryptocurrencies with technical utility or scarcity mechanisms:

Key Value Drivers:

- Viral content creation and meme propagation across social platforms

- Influencer endorsements creating buying frenzies with short-term price spikes

- Community coordination through Discord, Telegram, and Reddit channels

- Celebrity participation amplifying mainstream attention and adoption

Community Resilience Evidence:

Despite large PEPE whale sell-offs, retail buyers consistently stepped in to stabilize prices, demonstrating grassroots support that can counteract whale manipulation attempts. This dynamic suggests mature community development in leading meme coins like SHIB.

Financial and Economic Implications: Risk Assessment Framework

Volatility and Market Manipulation Risks

Meme coins exhibit extreme volatility due to limited intrinsic value and heavy dependence on market sentiment:

Risk Categories:

Price Manipulation Vulnerabilities:

- Pump-and-dump schemes orchestrated by coordinated whale groups

- Social media manipulation through fake news and coordinated shilling

- Low liquidity periods enabling significant price swings with relatively small trading volumes

Retail Investor Exposure:

- FOMO-driven investment decisions during viral price rallies

- Inadequate risk assessment due to limited financial literacy

- Emotional trading patterns leading to buy high, sell low behavior cycles

Systemic Risk Considerations:

While individual meme coin failures may not threaten financial stability, widespread retail losses could impact consumer spending and create political pressure for restrictive regulations.

Exchange Security and Asset Custody

The Kraken transfer highlights critical infrastructure supporting large-scale cryptocurrency operations:

Hot vs. Cold Storage Dynamics:

- Hot wallets: Connected to internet for active trading but vulnerable to cyber attacks

- Cold storage: Offline preservation providing enhanced security for long-term holdings

- Multi-signature protocols: Requiring multiple authorization keys for large value transfers

Institutional Security Standards:

Kraken’s wallet infrastructure demonstrates institutional-grade security practices essential for managing billions in digital assets while maintaining operational efficiency for millions of users globally.

Regulatory and Policy Perspectives: India’s Evolving Framework

Current Legal Status and Taxation Regime

India’s cryptocurrency regulatory approach reflects cautious pragmatism, avoiding outright bans while implementing deterrent taxation:

Tax Structure Implementation:

- Section 115BBH: 30% flat tax rate on all cryptocurrency gains

- Section 194S: 1% Tax Deducted at Source (TDS) on transactions exceeding ₹50,000 (₹10,000 in some cases)

- No loss offsetting: Crypto losses cannot offset other capital gains

- No foreign exchange benefits: Transactions treated as domestic for tax purposes kychub

Regulatory Authority Structure:

- Digital Currency Board of India (DCBI): Primary regulatory oversight

- Reserve Bank of India (RBI): Banking aspects and monetary policy implications

- Securities and Exchange Board of India (SEBI): Investment activity monitoring

- Ministry of Finance: Overall policy framework development

RBI’s Stance and Digital Currency Initiative

RBI Governor Shaktikanta Das has consistently expressed concerns about cryptocurrency’s impact on financial stability and monetary sovereignty:

Key Concerns Identified:

- Macroeconomic stability risks from uncontrolled capital flows

- Exchange rate volatility due to cryptocurrency speculation

- Monetary policy effectiveness compromised by alternative currency adoption

- Financial system integrity threatened by unregulated digital assets

Digital Rupee Development:

Union Minister Piyush Goyal confirmed India’s plan to launch an RBI-backed digital currency designed to:

- Simplify transactions and reduce paper currency dependence

- Enable faster, traceable payments with central bank guarantee

- Provide government-backed alternative to private cryptocurrencies

- Maintain monetary sovereignty while embracing digital innovation

Regulatory Challenges for Decentralized Assets

Meme coins like SHIB present unique regulatory challenges:

Decentralization Complexities:

- No central issuing authority to regulate or hold accountable

- Global trading across multiple jurisdictions complicating enforcement

- Anonymous trading capabilities hampering Know Your Customer (KYC) compliance

- Smart contract automation reducing regulatory control points

Enforcement Limitations:

- Peer-to-peer transfers occurring outside regulated exchange systems

- Decentralized exchange (DEX) trading bypassing traditional compliance mechanisms

- Cross-border arbitrage exploiting regulatory differences between countries

Regulatory and Policy Perspectives

Consumer Protection Framework

Retail investors face disproportionate risks in meme coin markets due to information asymmetries and limited regulatory protection:

Vulnerability Assessment:

- Limited financial literacy regarding blockchain technology and cryptocurrency fundamentals

- Susceptibility to social media influence and herd mentality trading

- Inadequate risk capital with many investors using borrowed funds or essential savings

- Emotional decision-making during extreme price volatility periods

Current Protection Gaps:

- No investor compensation schemes for cryptocurrency losses

- Limited dispute resolution mechanisms for trading platform issues

- Absence of mandatory risk disclosures in cryptocurrency marketing

- Weak cooling-off periods for impulsive investment decisions

Digital Literacy and Education Requirements

Successful cryptocurrency regulation requires comprehensive investor education addressing technical, financial, and risk management aspects:

Education Priority Areas:

- Blockchain technology fundamentals and cryptocurrency operation principles

- Wallet security practices and private key management

- Risk assessment frameworks for evaluating speculative investments

- Scam identification and fraud prevention strategies

Delivery Mechanisms:

- Mandatory education modules before cryptocurrency account activation

- Regular risk awareness campaigns through traditional and digital media

- School curriculum integration for digital financial literacy

- Professional development programs for financial advisors and bank staff

Investor Grievance and Redressal Systems

Establishing effective consumer protection requires robust complaint handling:

Proposed Framework Elements:

- Dedicated cryptocurrency ombudsman for investor complaints

- Mandatory grievance resolution timelines for exchange platforms

- Alternative dispute resolution mechanisms for trader-exchange disputes

- Consumer compensation funds financed through industry levies

Socio-Economic Concerns and Systemic Impact

Digital Divide and Financial Inclusion

Cryptocurrency adoption patterns reveal significant socio-economic disparities:

Access Barriers:

- High-speed internet requirements for real-time trading limiting rural participation

- Smartphone and computer costs creating technology access barriers

- English language dominance in trading platforms and educational materials

- Banking infrastructure requirements for fiat currency conversion

Wealth Inequality Amplification:

- Early adopter advantages benefiting technology-savvy urban populations

- High minimum investment amounts excluding low-income participants

- Sophisticated trading strategies requiring advanced technical knowledge

- Network effects favoring existing cryptocurrency communities

Potential Socio-Economic Impact of Losses

Large-scale retail losses from meme coin speculation could create broader economic and social consequences:

Household Impact:

- Reduced consumer spending from investment losses

- Increased household debt when borrowed funds are used for crypto speculation

- Family relationship stress from financial losses and risky investment decisions

- Retirement planning disruption when pension funds are diverted to crypto speculation

Community Effects:

- Reduced local business activity in communities with high crypto participation

- Increased demand for social services from financially distressed families

- Mental health impacts from sudden wealth loss and social pressure

Gender and Demographic Considerations

Cryptocurrency participation patterns show significant demographic skews:

Participation Analysis:

- Male-dominated trading communities with limited female participation

- Young adult concentration with older populations largely excluded

- Urban bias in cryptocurrency adoption and education access

- Higher income correlation with sustained crypto market participation

Lessons and Policy Recommendations

Strengthening Investor Protection Framework

Comprehensive consumer protection requires multi-layered intervention:

Immediate Priority Actions:

Enhanced Disclosure Requirements:

- Mandatory risk warnings on all cryptocurrency advertisements

- Standardized risk rating systems for different crypto asset categories

- Regular market risk updates during periods of extreme volatility

- Clear information about tax implications and regulatory status

Trading Platform Accountability:

- Minimum capital requirements for cryptocurrency exchanges

- Mandatory insurance coverage for customer fund protection

- Regular security audits and transparency reporting

- Restricted marketing practices targeting vulnerable populations

Regulatory Clarity and Framework Development

Effective governance requires balancing innovation encouragement with consumer protection:

Policy Framework Elements:

Risk-Based Regulation:

- Different regulatory standards for various cryptocurrency categories

- Higher scrutiny for high-risk assets like meme coins

- Streamlined processes for established cryptocurrencies with technical utility

- Regular framework updates responding to technological developments

Institutional Capacity Building:

- Specialized regulatory units with blockchain and cryptocurrency expertise

- International cooperation on cross-border enforcement

- Technology infrastructure for real-time market monitoring

- Research and development partnerships with academic institutions

Innovation and Economic Development Balance

Policy frameworks should encourage beneficial blockchain innovation while managing speculative risks:

Strategic Development Areas:

- Enterprise blockchain applications in supply chain management, healthcare, and government services

- Regulated digital asset categories supporting economic development goals

- Sandbox environments for fintech experimentation under controlled conditions

- Public-private partnerships for digital infrastructure development

International Cooperation and Standards Harmonization

Global cryptocurrency markets require coordinated regulatory approaches:

Cooperation Priorities:

- Information sharing agreements for cross-border enforcement

- Standardized regulatory frameworks reducing jurisdictional arbitrage

- Joint research initiatives on cryptocurrency market dynamics

- Technical standard harmonization for interoperability and consumer protection

Future Outlook and Strategic Implications

Emerging Market Trends

The meme coin ecosystem continues evolving with significant implications for policy makers:

Technology Integration Trends:

- DeFi protocol integration enabling complex financial products built on meme coin foundations

- Non-Fungible Token (NFT) ecosystems expanding meme coin utility beyond simple trading

- Cross-chain interoperability allowing meme coin trading across multiple blockchain networks

- Artificial intelligence integration for automated trading and market analysis

Market Maturation Indicators:

- Institutional participation through specialized meme coin funds

- Regulatory recognition in progressive jurisdictions

- Integration with traditional finance through custody services and investment products

- Mainstream adoption for payments and digital commerce applications

Policy Evolution Requirements

Regulatory frameworks must adapt to rapidly changing technological and market conditions:

Adaptive Governance Needs:

- Real-time monitoring capabilities for emerging risks and market manipulation

- Flexible regulatory standards allowing innovation while maintaining consumer protection

- International coordination on global market developments and regulatory best practices

- Stakeholder engagement including industry participants, consumer advocates, and technical experts

Conclusion: Navigating India’s Cryptocurrency Crossroads

The 512 billion SHIB transfer worth ₹63.4 crore represents more than a simple whale transaction – it symbolizes the growing sophistication and institutional interest in meme coin ecosystems that policymakers can no longer ignore. With recipient wallet accumulation reaching 1.47 trillion tokens and continued buying during market weakness, this event demonstrates genuine long-term conviction in speculative digital assets.

India’s regulatory response reflects pragmatic caution: 30% taxation and 1% TDS create significant barriers to speculative trading while avoiding outright bans that might stifle beneficial blockchain innovation. Union Minister Piyush Goyal’s emphasis on RBI-backed digital currency signals government commitment to digital payment evolution within controlled regulatory frameworks.

For UPSC aspirants and governance professionals, this dynamic illustrates fundamental challenges in 21st-century financial regulation. The tension between encouraging technological innovation and protecting vulnerable retail investors requires nuanced understanding of market dynamics, technological capabilities, and social impact.

The evidence is clear: meme coin markets are projected to reach $925.2 billion by 2035, representing a 26.7% annual growth rate that will reshape digital finance landscapes globally. India’s response – balancing heavy taxation with regulatory development – may become a model for emerging economies facing similar challenges.

Success requires comprehensive approaches: enhanced investor education, robust consumer protection frameworks, international regulatory cooperation, and continuous adaptation to technological evolution. The ₹63 crore whale transfer serves as a wake-up call – sophisticated investors are positioning for long-term growth in meme coin markets, and regulatory frameworks must evolve accordingly.

The stakes extend beyond financial markets: millions of retail investors seeking economic opportunity through cryptocurrency speculation deserve protection from predatory practices while maintaining access to legitimate investment opportunities. Achieving this balance will define India’s success in managing digital finance transformation.

+ There are no comments

Add yours