Key Highlights

- Finance Minister Nirmala Sitharaman emphasizes India must “prepare to engage” with stablecoins or risk exclusion from evolving monetary systems

- US GENIUS Act 2025 provides regulatory framework for stablecoins, positioning America as global leader in digital currency innovation

- India’s pilot CBDC (e-Rupee) reaches 5 million users across 15 banks, offering sovereign-backed alternative to private stablecoins

- Stablecoins present dual challenge: innovation opportunities versus risks of dollarization and monetary sovereignty loss

- RBI maintains cautious stance on cryptocurrencies while accelerating CBDC rollout to counter private digital currency threats

The Global Stablecoin Revolution

The digital finance landscape is witnessing unprecedented transformation as stablecoins emerge as powerful instruments bridging traditional banking and decentralized finance. Unlike volatile cryptocurrencies such as Bitcoin, stablecoins maintain stable value by pegging to reliable assets like the US dollar, making them ideal for payments, remittances, and cross-border transactions. statestreet

Global stablecoin market capitalization now exceeds $225 billion, with transaction volumes surpassing $6 trillion annually. The dominance is overwhelming – over 99% of stablecoins are USD-denominated, creating what experts term “digital dollarization” that could reshape global monetary dynamics.

The recent collapse of algorithmic stablecoin TerraUSD in May 2022, which lost its dollar peg and crashed to under $0.10, highlighted the inherent risks of poorly designed stability mechanisms. This event triggered broader market contagion, affecting other major stablecoins and demonstrating the fragility of unbacked algorithmic models.

America’s Strategic GENIUS Act Advantage

The United States has gained significant competitive advantage through the Guiding and Establishing National Innovation for US Stablecoins Act (GENIUS Act), signed into law by President Trump in July 2025. This bipartisan legislation establishes comprehensive federal framework for payment stablecoins, requiring: lw

Stringent Reserve Requirements: Stablecoin issuers must maintain 1:1 reserves in physical currency, US Treasury bills, and other low-risk approved assets

Licensed Issuer Framework: Only insured depository institutions, banks, credit unions, and Federal Reserve-approved nonbank institutions can issue stablecoins

Enhanced Consumer Protection: All issuers must comply with Bank Secrecy Act provisions, implementing robust anti-money laundering and counter-terrorism financing measures

The GENIUS Act takes effect January 2027 or 120 days after final implementing regulations, creating regulatory certainty that positions US stablecoins for global expansion.

India’s Current Cryptocurrency Conundrum

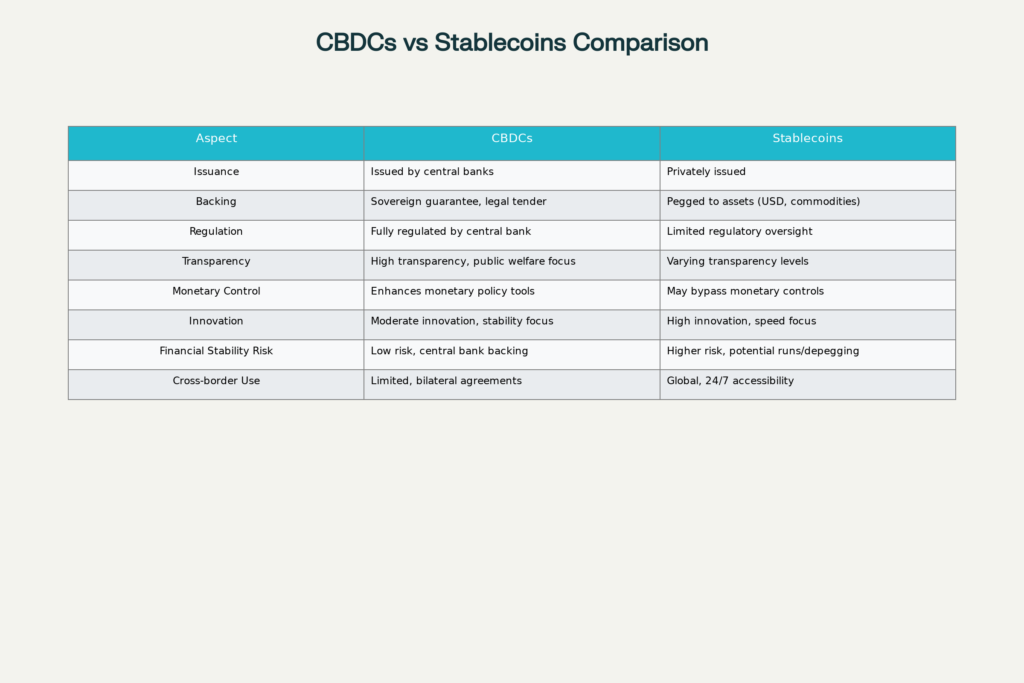

India maintains complex relationship with digital currencies, implementing 30% taxation on cryptocurrency gains while avoiding legal recognition. The Reserve Bank of India continues advocating outright bans on private cryptocurrencies, citing risks to financial stability and monetary sovereignty.

RBI’s Key Concerns:

- Financial Stability Risks: Cryptocurrencies could hamper monetary policy effectiveness and create systemic vulnerabilities

- Capital Flight Potential: Stablecoins enable bypassing traditional capital controls, potentially destabilizing domestic currency

- Regulatory Arbitrage: Cross-border digital assets present elevated supervisory challenges beyond traditional oversight mechanisms

Recent government documents reveal India’s inclination toward maintaining limited cryptocurrency oversight rather than comprehensive regulation, fearing that formal frameworks could legitimize potentially destabilizing assets.

The Digital Rupee Alternative

India’s Central Bank Digital Currency (e-Rupee) represents the nation’s strategic response to private stablecoin challenges. Launched in pilot phase during November 2022, the CBDC demonstrates impressive progress:

Current Metrics:

- 5 million users onboarded across retail and wholesale segments

- 15 participating banks including SBI, HDFC, ICICI, and others

- Peak of 1 million daily transactions achieved in December 2023

- 400,000+ merchants accepting digital rupee payments

The e-Rupee offers distinct advantages over private stablecoins through sovereign backing, legal tender status, and direct central bank control. Unlike UPI which facilitates bank-to-bank transfers, CBDC functions as actual digital currency stored in mobile wallets, enabling offline transactions and reducing systemic banking dependencies.

Strategic and Economic Implications

Finance Minister Sitharaman’s emphasis on “preparing to engage” with stablecoins reflects understanding of their disruptive potential and strategic implications for India’s monetary sovereignty. Key considerations include:

Monetary Sovereignty Risks: Dollar-backed stablecoins could accelerate unintended dollarization, particularly damaging for emerging markets where local currencies face displacement pressures. Countries experiencing elevated inflation or heavy reliance on cross-border payments prove especially vulnerable.

Capital Flow Disruption: Stablecoins enable circumventing traditional banking channels and capital controls, potentially impacting remittances, taxation collection, and macroeconomic management tools.

Policy Transmission Challenges: If USD-backed stablecoins become dominant settlement currencies for tokenized financial transactions, traditional monetary policy tools could lose effectiveness, further entrenching dollar dominance globally.

Financial Stability Concerns: Unchecked stablecoin proliferation may create systemic risks, including potential runs on issuers, financial contagion, and stability threats during market stress periods.

Global Regulatory Landscape

The Financial Stability Board (FSB), responding to G20 mandates, issued comprehensive recommendations for global stablecoin arrangements in July 2023. These high-level guidelines emphasize:

- Technology-Neutral Frameworks: Promoting consistent regulation across jurisdictions while supporting responsible innovation

- Comprehensive Oversight: Ensuring stablecoin activities face appropriate banking, payments, and securities regulation

- International Cooperation: Coordinated approaches addressing cross-border regulatory challenges

European Union’s Markets in Crypto-Assets Regulation (MiCAR) provides robust oversight framework, though questions remain about European stablecoin competitiveness against US regulatory clarity.

Policy Recommendations for India

India’s path forward requires balancing innovation opportunities with monetary sovereignty protection:

Regulatory Framework Development: Establish clear classification system for stablecoins – whether currencies, commodities, or securities – with appropriate licensing and reserve requirements.

CBDC Enhancement: Accelerate digital rupee rollout with user-friendly features, offline functionality, and widespread merchant adoption to provide viable alternative to private stablecoins.

International Cooperation: Engage actively with G20, FSB, and bilateral partners to shape global stablecoin governance standards preventing regulatory arbitrage.

Consumer Protection Measures: Implement transparency mandates, reserve adequacy requirements, and redemption guarantees for any permitted private stablecoin operations.

Dynamic Policy Adaptation: Monitor evolving global trends and adjust regulatory approaches to prevent exclusion from emerging monetary architectures while safeguarding national interests.

The Road Ahead

Finance Minister Sitharaman’s call for preparedness reflects India’s strategic understanding that stablecoins represent more than technological innovation – they constitute potential reshaping of global monetary order. Countries that fail to engage proactively risk marginalization from future financial systems.

India’s twin-track approach – developing robust CBDC capabilities while carefully considering stablecoin regulation – positions the nation to harness digital currency benefits while preserving monetary sovereignty. Success requires maintaining delicate balance between fostering innovation and protecting financial stability.

The next phase will determine whether India emerges as leader in sovereign digital currency adoption or finds itself navigating increasingly dollarized digital economy dominated by foreign stablecoin arrangements.

+ There are no comments

Add yours