Key Highlights

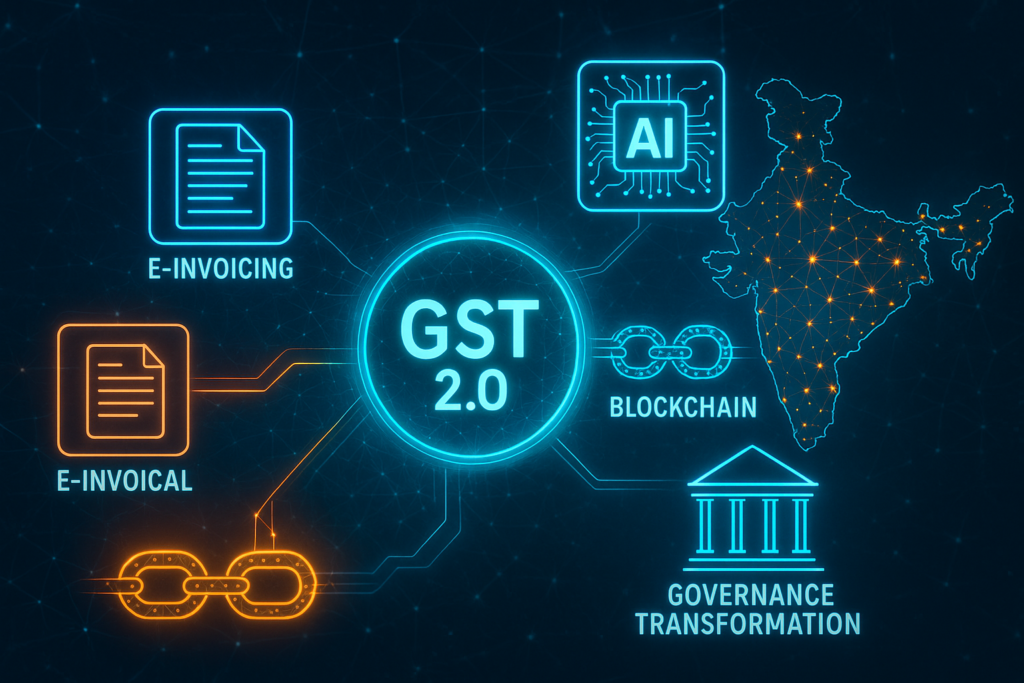

- GST 2.0 integrates advanced AI and blockchain technology creating real-time, transparent tax compliance ecosystem with 5x faster filing capabilities for professionals

- Constitutional framework through Articles 246A and 279A enables unique cooperative federalism model with 31 states pooling sovereign tax powers digitally

- E-invoicing system processes millions of transactions with mandatory implementation for ₹10+ crore businesses, generating IRN and QR codes for authentication

- MSME empowerment through digital simplification reduces compliance burden by 40% while providing mobile-friendly interfaces and multilingual support

- Revenue transformation achieved through reduced tax evasion, faster refunds (60+ days to 7-10 days), and enhanced economic formalization with 1.51 crore active registrations

As India strides toward its ambitious Digital India vision, the evolution of the Goods and Services Tax (GST) into GST 2.0 represents a paradigmatic shift from traditional tax administration to a technology-driven, real-time compliance ecosystem. Introduced through the 101st Constitutional Amendment Act (2016), GST has transformed from a “One Nation, One Tax” framework into a sophisticated digital governance model that leverages artificial intelligence, blockchain technology, and real-time data analytics to create transparent, efficient, and inclusive tax administration

Constitutional and Federal Foundation of Digital Tax Governance

Article 246A and 279A: Enabling Digital Federalism

The constitutional architecture underlying GST 2.0 rests on two foundational provisions that have revolutionized cooperative federalism in India’s digital age. Article 246A grants concurrent powers to both Parliament and State legislatures to legislate on GST, while Article 279A establishes the GST Council as a unique federal institution. civilsdaily

Constitutional Framework:

- Article 246A: Provides simultaneous powers for GST legislation to Centre and States

- Article 279A: Creates GST Council with Union Finance Minister as Chairman

- Voting mechanism: Centre has 1/3rd voting power, States collectively hold 2/3rd power

- Decision threshold: Requires three-fourths majority (minimum 25 out of 33 votes) for policy changes gstcouncil.gov

The Supreme Court’s landmark ruling in Union of India vs. VKC Footsteps (2021) emphasized that GST Council recommendations are “persuasive, not binding,” preserving the legislative sovereignty of both Centre and States while promoting “harmony as a postulate of cooperative federalism”.

Digital Federalism in Practice

The GST Council has successfully conducted 54 meetings since inception, making consensus-based decisions on rate structures, compliance procedures, and technological upgrades. This represents a unique experiment in digital governance where 31 independent states and Union Territories pool their sovereign indirect tax powers through technology-mediated cooperation.

Digital Governance Revolution Through GST 2.0

E-Invoicing and Real-Time Compliance

GST 2.0’s most transformative element is the mandatory e-invoicing system, which has created a real-time, transparent tax ecosystem. The system processes invoices through the Invoice Registration Portal (IRP), generating Invoice Reference Numbers (IRN) and QR codes for authentication.

E-Invoicing Implementation Scale:

- Mandatory for businesses with turnover above ₹10 crore (reduced from ₹20 crore)

- 30-day upload deadline enforced from April 1, 2025

- Integration with e-way bills and GSTR-1 returns for seamless compliance

- Real-time invoice matching reducing Input Tax Credit (ITC) disputes

Technological Infrastructure:

- Application Programming Interface (API) integration enabling direct ERP-to-GSTN communication

- Multi-Factor Authentication (MFA) mandatory for enhanced security

- Automated validation of GSTIN, HSN codes, and place of supply details

AI-Driven Compliance and Fraud Detection

Artificial Intelligence integration in GST 2.0 has revolutionized tax administration through predictive analytics and automated compliance monitoring:

AI Applications in GST:

- ADVAIT and BIFA systems: Government’s AI frameworks for Business Intelligence & Fraud Analytics

- Anomaly detection algorithms: Identify suspicious transaction patterns and fake invoicing

- Supplier risk scoring: AI models flag vendors with poor compliance history

- Automated reconciliation: Machine learning algorithms match invoices across multiple returns

Performance Impact:

Studies indicate AI-powered GST compliance tools enable 5x faster filing for Chartered Accountants, with automated reconciliation processing thousands of transactions in minutes compared to manual methods taking hours.

Blockchain Integration for Transparency

Blockchain technology is being integrated into GST 2.0 to ensure tamper-proof transaction records and enhance fraud prevention capabilities:

Blockchain Applications:

- Immutable transaction ledgers preventing invoice manipulation

- Smart contracts for automated tax calculation and compliance verification

- Decentralized validation reducing single points of failure

- Real-time audit trails enabling transparent transaction tracking

UPI-Blockchain Integration:

Research demonstrates that combining Unified Payments Interface (UPI) with blockchain technology creates secure, transparent payment ecosystems that complement GST 2.0’s digital infrastructure.

Economic and Fiscal Transformation Through Digitization

Revenue Mobilization and Tax Base Expansion

GST 2.0’s digital infrastructure has dramatically enhanced revenue collection and economic formalization:

Digital Impact on Revenue:

- Reduction in tax evasion through real-time transaction monitoring

- Improved Input Tax Credit flow eliminating artificial cash flow constraints

- Faster refund processing from 60+ days to 7-10 days through automation

- Enhanced compliance rates due to simplified digital filing procedures

Formalization of Economy:

The digital GST framework has driven significant economic formalization, with 1.51 crore active registrations as of 2025, including 1.32 crore normal taxpayers contributing to regular compliance.

Global Best Practices Integration

GST 2.0 incorporates international best practices from advanced digital tax systems:

Comparative Digital Tax Models:

- European Union VAT: Real-time transaction reporting and automated compliance verification

- Singapore GST digitization: API-based filing and electronic invoice validation

- Estonia’s X-Road system: Blockchain-based government services integration

Socio-Economic Dimension: Inclusion and Equity

MSME Empowerment Through Digital Simplification

GST 2.0 specifically addresses Micro, Small, and Medium Enterprise (MSME) challenges through technology-enabled simplifications:

MSME-Specific Digital Benefits:

- Simplified return filing reducing compliance burden by 40%

- Automated input tax credit calculations minimizing errors

- Mobile-friendly interfaces enabling compliance from remote locations

- AI-powered advisory services providing real-time guidance on tax obligations

Capacity Building Initiatives:

- Digital literacy programs for small traders and rural businesses

- Multi-language support in regional languages for broader accessibility

- Simplified compliance procedures for businesses with limited technical resources

Addressing Digital Divide Challenges

Rural and Small Business Integration:

- Offline-to-online transition support through government training programs

- Subsidized internet connectivity for tax compliance activities

- Simplified mobile applications requiring minimal technical expertise

- Community-based support centers providing digital assistance

Cybersecurity and Data Protection:

GST 2.0 implements robust cybersecurity measures including multi-factor authentication, encrypted data transmission, and regular security audits to protect taxpayer information.

Challenges and Implementation Roadmap

Technology Infrastructure Gaps

Current Limitations:

- GSTN portal overload during peak filing periods affecting user experience

- Internet connectivity issues in rural areas limiting digital access

- Technical skill gaps among small businesses requiring additional training

- Integration complexity between various ERP systems and GSTN APIs

Compliance Cost Considerations

Recent studies indicate 10.3% increase in compliance costs post-GST amendments, with businesses spending additional ₹4.16 thousand annually on digital compliance requirements. However, this investment yields significant long-term benefits through reduced errors, faster processing, and enhanced audit readiness.

Future Roadmap: Advanced Digital Integration

Next-Generation Technologies

Emerging Technology Integration:

- Machine Learning algorithms for predictive tax assessment and compliance guidance

- Natural Language Processing enabling voice-based query resolution

- Internet of Things (IoT) integration for real-time transaction monitoring

- 5G connectivity ensuring seamless digital filing across geographic locations

Policy Evolution and Governance Enhancement

Continuous Digital Transformation:

- Real-time policy adjustments based on AI-powered economic data analysis

- Predictive governance models anticipating taxpayer needs and system requirements

- Integrated government services connecting GST with other digital governance platforms

- International digital tax coordination for cross-border transaction management

GST 2.0 as Catalyst for $5 Trillion Digital Economy

Economic Growth Acceleration

GST 2.0’s technology-driven approach positions India to achieve its $5 trillion economy target by facilitating:

Growth Enablers:

- Reduced transaction costs through automated compliance procedures

- Enhanced business confidence via transparent, predictable tax administration

- Improved ease of doing business through digital-first governance approach

- Faster economic formalization bringing informal sector into mainstream economy

Innovation Ecosystem Development

Technology Sector Growth:

- Fintech innovation driven by API-based GST integration requirements

- Software development for compliance automation and business intelligence

- Cybersecurity solutions for protecting sensitive financial data

- Data analytics services providing business insights from GST transaction data

Global Leadership in Digital Tax Administration

GST 2.0 positions India as a global leader in digital tax administration, demonstrating how large-scale, complex federal systems can successfully implement technology-driven governance reforms. The model provides valuable lessons for other developing economies seeking to modernize tax administration while maintaining federal balance and inclusive growth.

International Recognition:

- World Bank acknowledgment of GST as one of the most ambitious indirect tax reforms globally

- OECD studies highlighting India’s innovative approach to digital tax compliance

- Bilateral cooperation agreements for sharing GST technology and best practices with other countries

Conclusion: Building Inclusive Digital Governance

GST 2.0 represents far more than tax reform – it embodies India’s commitment to building inclusive, technology-enabled governance that balances efficiency with equity, innovation with accessibility, and federal cooperation with local autonomy. By successfully integrating artificial intelligence, blockchain technology, and real-time data analytics with constitutional federalism, GST 2.0 demonstrates that large-scale digital transformation can be achieved while preserving democratic principles and ensuring inclusive participation.

The journey from fragmented indirect taxation to unified digital compliance showcases India’s capacity for transformative governance innovation. As the system continues evolving, GST 2.0 will remain a cornerstone of Digital India, enabling the nation to achieve its economic aspirations while strengthening democratic institutions and promoting social justice through technology-enabled governance.

The success of GST 2.0 in balancing technological advancement with constitutional federalism provides a blueprint for future governance reforms, demonstrating that digital transformation can strengthen rather than weaken democratic institutions when implemented with careful attention to inclusion, equity, and federal balance.

Mains

Q1. Discuss the role of GST 2.0 in promoting Digital India. How does it balance cooperative federalism with the goals of transparency and ease of doing business?

Q2. “GST 2.0 is not merely a tax reform but a digital governance framework.” Examine this statement in the context of India’s economic growth and fiscal federalism.

+ There are no comments

Add yours