Key Highlights

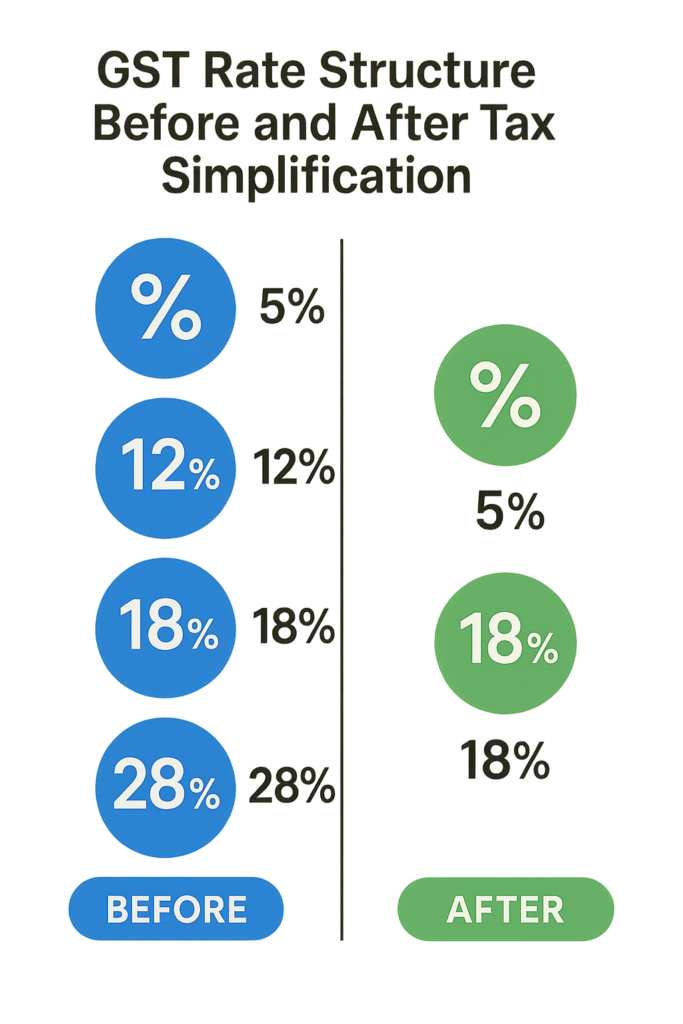

- GST 2.0 simplifies tax structure from complex 4-slab system to streamlined 3-tier framework (5%, 18%, 40%) effective September 22, 2025

- Record collections of ₹22.08 lakh crore in FY 2024-25 demonstrate GST’s success with 9.4% growth and average monthly collections of ₹1.84 lakh crore

- Comprehensive relief package reduces taxes on daily essentials, healthcare, education while introducing 40% rate for sin and luxury goods

- Digital transformation enhanced through AI-powered systems, blockchain integration, and simplified compliance procedures especially benefiting MSMEs

- Petroleum and alcohol remain excluded from GST framework due to constitutional constraints and revenue protection concerns for federal and state governments

Eight years after India’s Goods and Services Tax (GST) implementation on July 1, 2017, the nation stands at the threshold of its next transformative phase with GST 2.0. The comprehensive reforms, effective from September 22, 2025, represent the most significant overhaul of India’s indirect tax system since its inception. With record-breaking collections of ₹22.08 lakh crore in FY 2024-25 – a remarkable 9.4% year-on-year growth – GST has proven its potential to revolutionize tax administration while driving economic formalization. pib.gov

The Pre-GST Fragmentation and Historic Implementation

Legacy of Complex Indirect Taxation

Before GST’s revolutionary introduction, India’s indirect tax system resembled a complex labyrinth of 16 different taxes imposed by Central and State governments. This fragmented structure included excise duty, service tax, VAT, Central Sales Tax (CST), octroi, entry tax, and luxury tax, creating a cascading effect where “tax was levied on tax”.

Pre-GST Challenges:

- Multiple tax checkpoints causing logistics delays and compliance burden

- Cascading taxation effect inflating final consumer prices artificially

- Lack of input tax credit integration across different tax categories

- Interstate trade barriers hindering the “One Nation, One Market” vision

- Complex compliance requirements with multiple authorities and procedures

Constitutional Foundation and Federal Architecture

The 101st Constitutional Amendment Act, 2016 laid the groundwork for GST through Article 279A, establishing the GST Council as a federal fiscal institution with unprecedented cooperative federalism mechanisms.

The amendment introduced a dual GST model unique to India’s federal structure:

GST Structure Components:

- Central GST (CGST): Levied by Central Government on intrastate supplies

- State GST (SGST): Imposed by State Governments on intrastate transactions

- Union Territory GST (UTGST): Applied in Union Territories

- Integrated GST (IGST): Governing interstate transactions and imports journalijar

GST 1.0 Achievements: Transforming India’s Tax Landscape

Record Revenue Performance and Economic Formalization

GST’s performance trajectory demonstrates remarkable success in revenue generation and economic formalization. The system has achieved unprecedented collection milestones, with monthly collections consistently crossing ₹1.5 lakh crore and reaching historic peaks of ₹2.37 lakh crore in April 2025. saginfotech

Collection Milestones (2020-21 to 2024-25):

- 2020-21: ₹11.37 lakh crore (monthly average: ₹95,000 crore)

- 2021-22: ₹14.83 lakh crore

- 2022-23: ₹18.08 lakh crore

- 2023-24: ₹20.18 lakh crore

- 2024-25: ₹22.08 lakh crore (monthly average: ₹1.84 lakh crore) pib

Digital Infrastructure and Compliance Enhancement

GSTN Portal Revolution:

- 1.51 crore active GST registrations as of April 2025

- 1.32 crore normal taxpayers contributing to regular compliance

- 14.86 lakh composition taxpayers benefiting from simplified procedures

- 3.71 lakh TDS entities ensuring systematic tax deduction

E-way Bill System Success:

- Streamlined interstate goods movement reducing transit time by 30-40%

- Digital invoice matching enhancing transparency and reducing tax evasion

- Real-time tracking capabilities improving logistics efficiency across supply chains

GST 2.0: The Next Generation Tax Reform

Revolutionary Rate Rationalization

GST 2.0 introduces the most comprehensive rate rationalization since inception, transitioning from a complex 4-slab structure (5%, 12%, 18%, 28%) to a simplified 3-tier system (5%, 18%, 40%).

New Rate Structure Overview:

- 5% slab: Essential goods including food items, healthcare products, and basic necessities

- 18% slab: Standard goods and services forming the backbone of economic activity

- 40% slab: Sin goods and luxury items including tobacco, premium automobiles, and high-end consumer durables

Items Moving to Lower Tax Brackets:

- Daily essentials: Hair oil, shampoo, toothpaste (18% → 5%)

- Dairy products: Butter, ghee, cheese (12% → 5%)

- Healthcare: Individual health insurance (18% → Nil)

- Education: Exercise books, pencils, maps (12% → Nil)

- Automobiles: Small cars, motorcycles ≤350cc (28% → 18%)

- Electronics: Air conditioners, TVs >32″ (28% → 18%)

Digital Transformation and Compliance Simplification

Technology Integration Advances:

- Multi-Factor Authentication (MFA) mandatory for GSTN portal access enhancing security

- AI-powered invoice matching reducing discrepancies and processing time

- Blockchain integration for tamper-proof transaction records

- Automated refund processing reducing waiting periods from months to weeks

MSME Relief Measures:

- Simplified return filing procedures reducing compliance burden by 40%

- Reduced filing frequency for small taxpayers

- Enhanced input tax credit flow mechanisms

- Sector-specific clarifications for real estate and e-commerce

Challenges and Ongoing Exclusions

Petroleum and Alcohol: The Persistent Omissions

Despite calls for comprehensive inclusion, petroleum products and alcoholic beverages remain outside GST purview even in the 2.0 framework. Finance Minister Nirmala Sitharaman confirmed that “petroleum and alcohol will not come under GST in the near future”.

Constitutional and Political Constraints:

- Article 366(12A) specifically excludes alcohol for human consumption from GST definition

- Entry 54 of State List allows states to continue levying VAT on petroleum products

- Revenue protection concerns for both Central and State governments

- Fiscal autonomy preservation preventing states from losing major revenue sources taxo

Implementation Challenges and MSME Impact

Compliance Cost Analysis:

Recent studies indicate GST compliance costs increased by 10.3% post-amendments, from ₹40.27 thousand to ₹44.43 thousand for businesses. Monthly filing time increased to 10.22 hours on average, with businesses receiving 3.13 notices from GST departments over six months.

Federal Friction Points:

- Centre-State disputes over compensation mechanisms

- Revenue sharing complexities during economic downturns

- Rate determination disagreements in GST Council meetings

- Implementation timeline coordination across different state administrations

Global Benchmarking and International Learning

Comparative Models and Best Practices

Canada’s Dual GST Success:

Canada’s Harmonized Sales Tax (HST) system combining federal GST with provincial sales taxes provides valuable lessons for India’s federal structure integration.

Australia’s Uniform Rate Approach:

Australia’s 10% uniform GST rate demonstrates simplicity benefits, though India’s diverse economic structure requires differentiated taxation.

European Union’s VAT Framework:

The EU’s Value Added Tax system with standard rates between 17-27% across member countries offers insights for rate harmonization while maintaining sovereignty.

Economic Impact and Growth Implications

Inflation Reduction and Consumer Relief

GST 2.0 Economic Benefits:

Economists project inflation reduction of up to 1.1 percentage points due to lower taxes on essential goods and consumer durables. The reforms are expected to boost consumption demand especially in automobiles, consumer durables, and FMCG sectors.

Revenue Impact Assessment:

The government anticipates short-term revenue loss of ₹48,000 crore but expects this to be offset by increased demand, broader tax compliance, and enhanced economic activity in the medium term.

Sectoral Winners and Economic Transformation

Beneficiary Sectors:

- Automobile industry: Significant cost reduction for small cars and two-wheelers

- FMCG and consumer durables: Lower input costs boosting affordability

- Healthcare and education: Enhanced access through tax exemptions

- Agriculture and farming: Reduced equipment costs supporting modernization

GST Council: Federal Fiscal Institution

The GST Council, established under Article 279A, represents a unique experiment in cooperative federalism with the Union Finance Minister as Chairman and State Finance Ministers as members. This institution has successfully navigated complex federal negotiations while maintaining consensus-based decision making.

Council Achievements:

- 54 meetings since inception addressing rate structures, procedural issues, and policy reforms

- Unanimous decisions on major policy changes despite diverse state interests

- Effective dispute resolution mechanisms preventing federal conflicts

- Balanced revenue sharing ensuring both Central and State fiscal needs

Technology and Future Roadmap

AI and Blockchain Integration

Next-Generation Digital Infrastructure:

- Artificial Intelligence deployment for fraud detection and risk assessment

- Machine Learning algorithms for pattern recognition in tax evasion

- Blockchain technology ensuring transaction authenticity and preventing manipulation

- Real-time data analytics enabling predictive policy making

Compliance Automation and Efficiency

Automated Processes:

- Invoice matching automation reducing manual intervention by 80%

- Refund processing acceleration from 60+ days to 7-10 days

- Risk-based assessment targeting high-risk taxpayers for scrutiny

- Seamless input tax credit flow across supply chains

Environmental and Social Impact

Sustainable Taxation Framework

Green Tax Initiatives:

- Lower rates on electric vehicles encouraging clean transportation

- Reduced taxes on solar equipment supporting renewable energy adoption

- Environmental compliance integration with tax assessment procedures

- Carbon footprint considerations in rate determination

Social Equity and Inclusive Growth

Progressive Tax Structure:

- Essential goods protection through 5% rate or exemptions

- Luxury goods taxation at 40% ensuring progressive burden distribution

- MSME support measures reducing compliance costs and complexity

- Rural economy integration through simplified procedures

Looking Ahead: The Future of Taxation in India

GST 2.0 represents more than tax reform – it embodies India’s commitment to building a modern, efficient, and equitable taxation system that supports the nation’s economic aspirations while ensuring social justice. The journey from a fragmented indirect tax regime to a unified digital platform showcases India’s capacity for transformative governance reform.

Future Priorities:

- Complete digitization of tax administration reducing human interface

- Predictive analytics for economic policy formulation and monitoring

- International coordination for cross-border digital taxation

- Continuous simplification based on taxpayer feedback and global best practices

The success of GST 2.0 will be measured not just in revenue collection statistics but in its ability to facilitate ease of doing business, promote economic formalization, and support India’s journey toward becoming a $5 trillion economy. As the nation celebrates eight years of GST implementation, the transition to GST 2.0 marks a matured taxation system ready to support India’s next phase of economic growth and global competitiveness.

The evolution continues, and with each reform, India moves closer to achieving the original vision of “One Nation, One Tax, One Market” – a dream that seemed impossible in the pre-GST era but is now becoming a tangible reality shaping India’s economic future.

🔹 Mains Questions

- GS-II: “GST Council has emerged as a federal institution balancing Centre-State fiscal relations. Critically examine.”

- GS-III: “GST 2.0 must focus on rate rationalisation and widening of the tax base rather than incremental fixes. Discuss.”

+ There are no comments

Add yours