India is riding a tidal wave of digital transformation. Nowhere is this more clear than in the electrifying rise of digital payments, especially via the Unified Payments Interface (UPI). Used by everyone from street vendors in small towns to luxury malls in metros, UPI has put the power of cashless transactions into the palm of every Indian. But while these advances are remarkable, the full promise of Digital India will only be realized if we close critical gaps in awareness, financial literacy, and digital infrastructure—ensuring that progress doesn’t leave anyone behind.

The UPI Boom: Changing India’s Payment Landscape

Launched in 2016, the Unified Payments Interface (UPI) has soared to become one of the world’s largest and fastest-growing digital payment ecosystems. In 2023 alone, Indians made over 100 billion UPI transactions, a feat few other nations can match. From paying for a cup of chai at a roadside stall to splitting bills via QR codes, digital transactions are now an everyday reality across social and economic divides. NPCI: UPI Official Portal

What Fuels UPI’s Success?

- Simplicity: Seamless, real-time transfers using just a mobile number, QR, or virtual address.

- Interoperability: One interface works across 300+ banks and numerous financial apps.

- Low Cost: Near-zero transaction fees, supporting businesses both big and small.

- Security: With features like two-factor authentication and built-in fraud detection.

Challenging the Digital Divide

Despite these achievements, the surge in usage masks persistent disparities:

1. Awareness and Financial Literacy

While UPI is intuitive, millions remain outside its reach due to lack of basic digital and financial know-how—especially in rural and semi-urban areas, among the elderly, and marginalized communities.

- Digital literacy remains patchy; the gender gap in mobile phone and digital account access is real.

- Many first-time users fear scams or mistrust digital banking.

2. Infrastructure Gaps

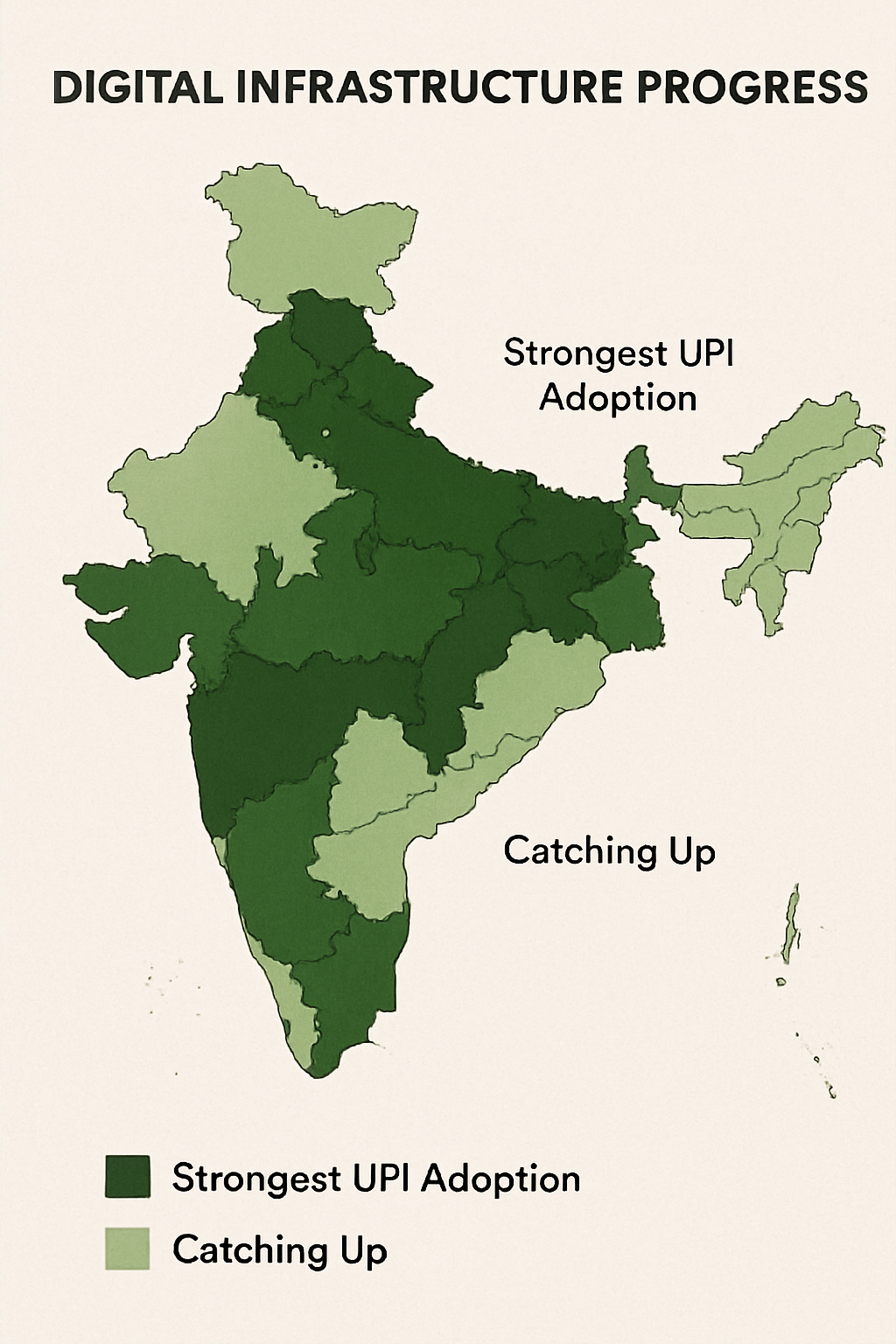

Reliable high-speed internet and smartphone access are not universal across India. In interior regions, patchy networks and device affordability continue to limit participation.

- Infrastructure challenges persist in the northeast, hill states, and the tribal belts.

- Stable electricity and mobile connectivity are still developing in some regions.

3. Trust and Security

While UPI’s security features are robust, there’s been an uptick in phishing, social engineering, and digital fraud. Financial literacy is critical for recognizing and avoiding scams.

Inclusive Strategies: Closing the Gap

Digital India was built on the principle of inclusivity—making government and financial services accessible to all. How do we carry this spirit into the next phase of the digital payments revolution?

1. Expand Digital and Financial Literacy

- Empower rural communities, women, and senior citizens with targeted campaigns and local language materials.

- Deploy digital and financial literacy workshops through schools, panchayats, and SHGs.

- Encourage “train the trainer” models, using local youth as digital ambassadors.

2. Invest in Infrastructure

- Accelerate BharatNet and related programs to deliver high-speed internet to every village.

- Expand affordable smartphone schemes and digital kiosks.

- Ensure continuous improvement in cybersecurity, connectivity, and platform reliability.

3. Promote Inclusive Design

- Develop payment apps with simple interfaces, multi-language support, and features for the visually or hearing impaired.

- Collaborate with fintech innovators and banks to create customized solutions for unbanked or underserved segments.

4. Strengthen Trust and Safety

- Publicize UPI safety features, fraud hotline numbers, and grievance redressal mechanisms.

- Regularly update and audit systems to limit vulnerabilities.

The Road Ahead: Collaboration, Policy, and Private Sector Drive

India’s digital payments ecosystem is envied worldwide, but it won’t be complete until every citizen—regardless of location, gender, or education—can participate with confidence and security. That’s only possible through robust collaboration:

- Government: Policy, investment, and public awareness campaigns

- Industry: Innovative, inclusive, and accessible tech solutions

- Civil Society: Local training, advocacy, and feedback to shape user-friendly tools

Conclusion: Toward a Truly Inclusive Digital Economy

The UPI-powered digital payments boom is transformative, but its benefits must reach every Indian. By doubling down on literacy, infrastructure, safety, and inclusivity, we can transform Digital India from a slogan to a shared reality. Only then will India’s leap into a cashless economy also be a leap toward true financial inclusion, equity, and empowerment.

+ There are no comments

Add yours